Subscribe to Bankless or sign in

![]() Hyperliquid is the most contested property in crypto right now. Spot HYPE ETFs from 21Shares and Bitwise launched on U.S. exchanges last week. Grayscale and VanEck are close behind. Underneath that institutional rush sits a longer-running scramble to claim a piece of the exchange's economics.

Hyperliquid is the most contested property in crypto right now. Spot HYPE ETFs from 21Shares and Bitwise launched on U.S. exchanges last week. Grayscale and VanEck are close behind. Underneath that institutional rush sits a longer-running scramble to claim a piece of the exchange's economics.

Last fall, Hyperliquid ran an open RFP for a native stablecoin called USDH, designed to recapture the revenue it had been leaking to ![]() Coinbase and Circle. Roughly $5.6B in USDC sat inside the exchange's bridge, generating around $200M annually in interest that flowed to its centralized competitor. None of it returned to the platform actually driving the demand. Native Markets won the community vote over bids from Paxos, Ethena, and others, and USDH went live.

Coinbase and Circle. Roughly $5.6B in USDC sat inside the exchange's bridge, generating around $200M annually in interest that flowed to its centralized competitor. None of it returned to the platform actually driving the demand. Native Markets won the community vote over bids from Paxos, Ethena, and others, and USDH went live.

Then, last week, Native Markets sold USDH to Coinbase, agreeing to sunset the aligned stablecoin and see USDC reinstalled as the primary quote asset on the exchange, in exchange for 90% of revenue flowing back to Hyperliquid (though exact capture mechanics remain unclear). The deal was read as a win for Hyperliquid at the expense of Coinbase and Circle. That read’s understandable, but inaccurate.

What Hyperliquid gets out of the deal is clear: a sharply improved revenue split (roughly double what they were making with USDH), regulatory firepower via alignment with crypto's largest voice in DC, the UX benefits of returning to the trusted stablecoin the exchange was already built around and that is predominantly used in the HIP-3 markets which have garnered Hyperliquid all its headlines over the past six-ish months.

The Coinbase and ![]() Circle side was read as an optics boost, a way to align with one of the most crypto-native and successful projects of last cycle. But put USDC's actual market positioning next to the growth trajectory of perpetuals, and a second beneficiary comes into view.

Circle side was read as an optics boost, a way to align with one of the most crypto-native and successful projects of last cycle. But put USDC's actual market positioning next to the growth trajectory of perpetuals, and a second beneficiary comes into view.

Coinbase and Circle are getting distribution for USDC at a scale that may matter more than anything else in the deal.

My read: Coinbase x Circle get defense and new growth vector against USDT, essentially the aligned quote asset for Binance

— David Christopher (@davewardonline) May 14, 2026

Hyperliquid gets regulatory firepower and revenue, tho exact amount remains unclear — but higher than before. https://t.co/NuWIkPxP76

How Are Things at Home?

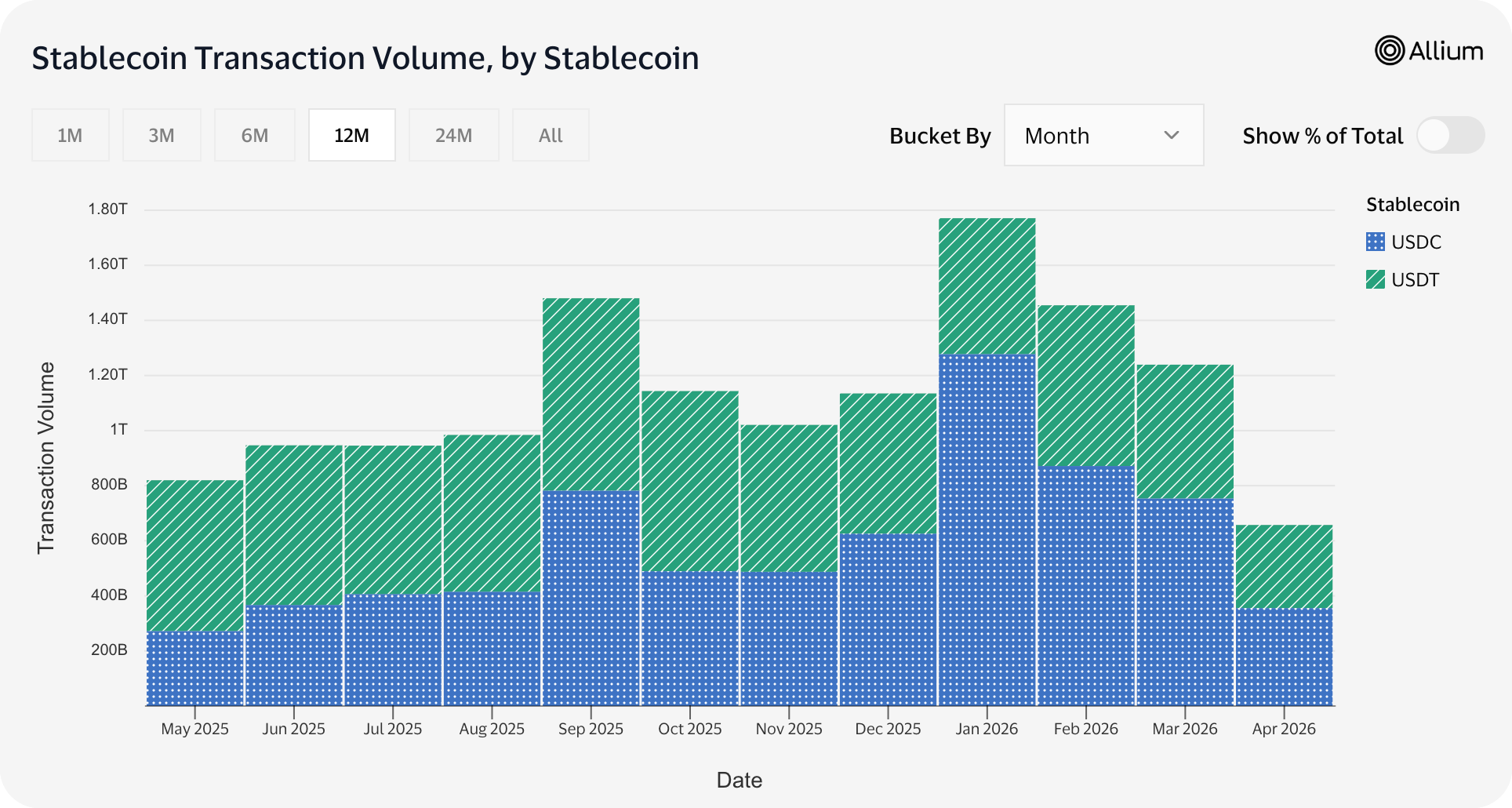

USDC has shown real momentum since GENIUS passed. Circle was pre-positioned for the regulatory world the framework created, with USDC being U.S.-based and compliance-forward. That positioning has translated into volume. Allium data shows USDC transaction volume reached $355B in May 2026, surpassing USDT for the first time in recent months and reflecting accelerating growth since GENIUS passed last July.

What hasn't moved is the structural picture. In April 2025, just before GENIUS, USDT held 67% of the stablecoin market and USDC held 27.6%. A year later, USDT sits at 67.3% and USDC at 28.1%. Half a percentage point of movement. Supply share is flat even as USDC's transaction volume accelerates.

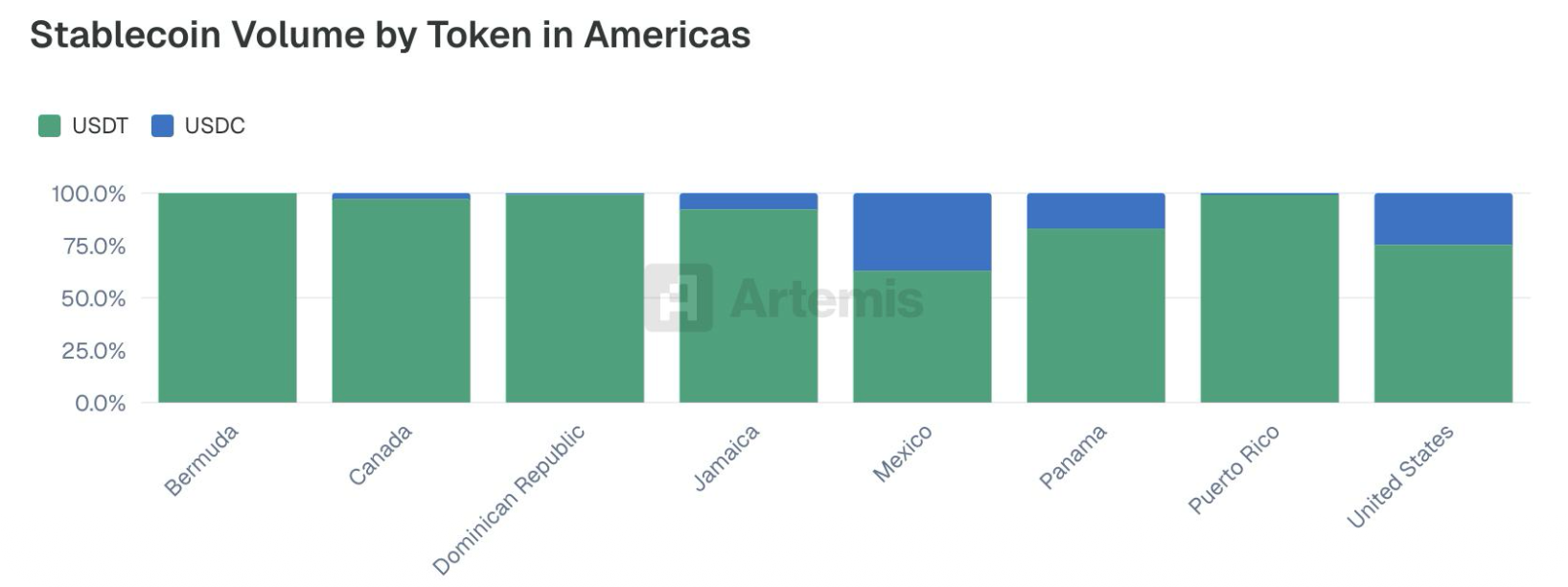

Reports from last October had the U.S. as USDC’s strongest market and, given the correlation between growth post GENIUS, it’s safe to say the U.S. has been the largest point of growth for USDC. Yet, it's also exactly where new competition is concentrating. Stripe decisively entered the stablecoin business with Tempo and other acquisitions. Major financial institutions are launching their own GENIUS-compliant domestic stables, all encroaching on USDC's main market.

And USDC has no real foothold abroad to fall back on if the domestic squeeze tightens. Almost everywhere else, USDT dominates as the default dollar, used for saving, investing, and trading, and continues to expand aggressively. Multiple new chains have launched over the past year specifically to extend USDT distribution, and ![]() Tether introduced USAT to attack USDC inside the U.S. regulatory perimeter under GENIUS compliance.

Tether introduced USAT to attack USDC inside the U.S. regulatory perimeter under GENIUS compliance.

Coinbase and Circle have real momentum to extend, and a narrow window to lock in distribution before competition ramps up. Trading, particularly perpetuals, is the venue to do it.

Perpetuals Are the Arena

Alongside stablecoins, perpetuals are one of the fastest growing categories in crypto, continually posting double to triple digit year-over-year growth.

Enjoying this article?

Subscribe to Bankless or sign in

They're structurally intertwined with stablecoins, which predominantly serve as the quote asset perp markets are built against. USDT already holds a major foothold here, as the primary quote asset for the majority of markets on the largest perpetuals exchange globally, Binance. Anyone trading Binance's biggest markets does so primarily with USDT, which helps secure USDT supply on the exchange, in turn having obvious downstream pull on deposits, withdrawals, and onchain activity around the exchange.

While, Hyperliquid does much less volume than Binance, it is the largest perpetuals exchange onchain, holding 30% of total onchain perpetuals market share and commanding 46% of open interest, positions that have held up against repeated attempts to compete with it.

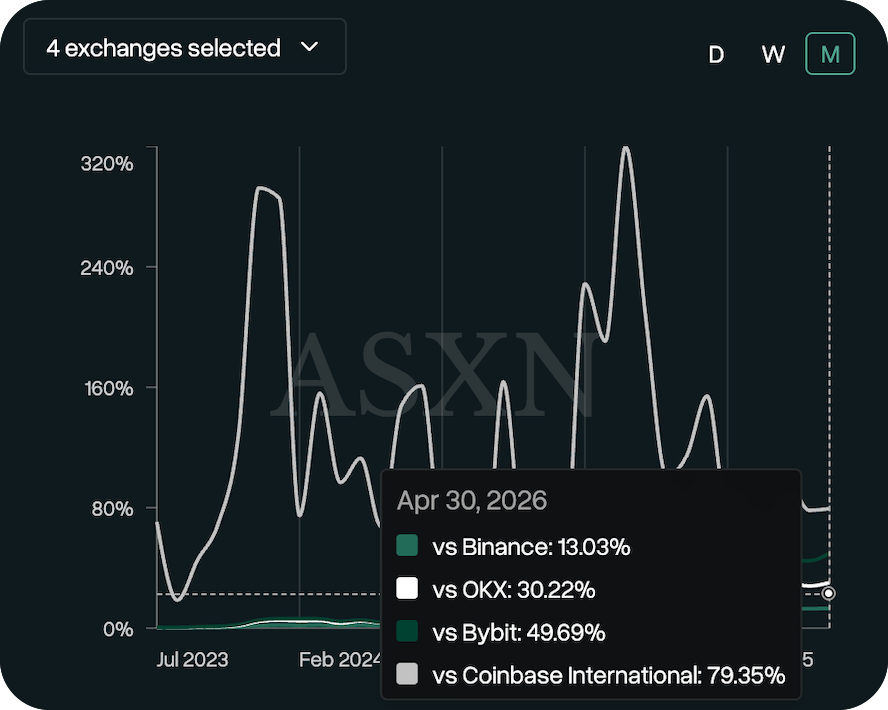

And, while it’s not centralized, it’s clearly competing on equal footing, running at ~50% of Bybit's volume, ~30% of OKX's volume, ~79% of Coinbase International's volume, as of April 30th. All this amounted to only ~13% of Binance's volume, yet it’s a number which continues to increase with trajectory pointing only one direction.

While still early, Hyperliquid's dominance in onchain perpetuals, rivaling and sometimes surpassing centralized exchange volume, positions it with global reach comparable to Binance's footprint outside the U.S., in turn opening up a channel for Coinbase and Circle to compete with Tether and turn Hyperliquid into a structural distribution channel for USDC.

Coinbase Picks Its Lane

This, though, raises the question of why wouldn’t Coinbase simply build that distribution channel itself by building out its perpetuals offerings further?

Because Coinbase is beholden to a regulatory framework that limits how many customers it can serve and how many markets it can launch. Currently Coinbase reaches roughly 100 countries, a little more than half of Binance’s 180. Hyperliquid can reach even more thanks to its more “permissive” environment, giving it an edge over both ![]() Binance and Coinbase, one Coinbase couldn’t hope to replicate.

Binance and Coinbase, one Coinbase couldn’t hope to replicate.

So Coinbase and Circle let Hyperliquid carry the global reach while USDC rides along underneath. The deal captures the upside through USDC supply growth and the revenue that comes with it, without Coinbase having to fight a jurisdictional battle it can't win. A slice of the economics, but a slice at a scale they can't reach on their own.

Tether Trying Same Playbook

Tether's running their own version of this, though on a much smaller scale. After April's Drift exploit, Tether committed up to $147.5M to its recovery, a deal which installed USDT as Drift's settlement asset, established a Tether-backed USDT facility for designated market makers, and funded a trading incentive layer.

In other words, Tether used the Drift crisis to flip the base currency of a major  Solana perp DEX. USDC had more than 2x USDT's stablecoin presence on Solana before the deal, a dynamic prevalent across the entire chain. Both sides of the stablecoin war have figured out the same thing: perpetuals are a critical battleground for stablecoins.

Solana perp DEX. USDC had more than 2x USDT's stablecoin presence on Solana before the deal, a dynamic prevalent across the entire chain. Both sides of the stablecoin war have figured out the same thing: perpetuals are a critical battleground for stablecoins.

Today, Drift is announcing a collaboration with @tether and other partners totaling up to nearly $150 million to support our commitment to a relaunch with USDT at the center, and a path to user recovery.

— Drift (@DriftProtocol) April 16, 2026

These funds encompass a $100M revenue-linked credit facility, an ecosystem…

Overall, to capitalize on the momentum GENIUS gave them, Coinbase and Circle need more distribution and the Hyperliquid deal could be that: letting USDC spread on the primary venue for onchain trading, in a category growing faster than almost anything else in crypto, with the ability to compete on the same scale that USDT and Binance do.

It may also be a bet on the domestic perimeter opening. CFTC Chair Selig has been explicit about wanting perpetuals available in the U.S., which CLARITY's passage could ensure. Reporting this week indicates the SEC is preparing an "innovation exemption" under the agency's Project Crypto initiative that would let crypto-native platforms offer onchain trading of tokenized U.S. equities under lighter registration requirements. Between Selig's CFTC posture and Atkins's SEC push, it looks like Coinbase is positioning early, having Hyperliquid gain U.S. distribution with USDC already installed.

This is all speculation, but it tracks with how Wall Street and institutional players are likely to view Hyperliquid: as their entry point into the coming perpetuals regime. That's about as compelling a tailwind as an asset can have.