Sponsor: Brix — Access real-world yield in DeFi. Built on MegaETH.

- 👋

Ethereum Foundation Members Josh Stark, Trent Van Epps Resign. The pair announced their resignations from the EF earlier this week, but didn't offer up any reasons for the departures.

Ethereum Foundation Members Josh Stark, Trent Van Epps Resign. The pair announced their resignations from the EF earlier this week, but didn't offer up any reasons for the departures. - 👁️🗨️ Tinder, DocuSign, Zoom Integrate Sam Altman’s World ID for Proof-of-Humanity Verification. Major services are embracing biometric identity to fight AI-driven fraud.

- 🐙

Kraken Eyes Bitnomial Buyout in $550M Cash & Stock Deal. The impending purchase marks the crypto exchange's seventh acquisition since the start of 2025.

Kraken Eyes Bitnomial Buyout in $550M Cash & Stock Deal. The impending purchase marks the crypto exchange's seventh acquisition since the start of 2025.

| Prices as of 6pm ET | 24hr | 7d |

|

Crypto $2.56T | ↗ 3.0% | ↗ 5.9% |

|

BTC $77,444 | ↗ 3.2% | ↗ 5.9% |

|

ETH $2,429 | ↗ 3.8% | ↗ 7.9% |

In what has already been a very unpredictable year, I’m perhaps most shocked by the (very small, incredibly mild) pangs of sympathy I am feeling this week for His Excellency Justin Sun.

On Tuesday, my colleague Jack wrote about the ![]() Tron billionaire’s feud with the Trump-founded lending platform World Liberty Finance, which he had invested at least $75M into before having his assets locked.

Tron billionaire’s feud with the Trump-founded lending platform World Liberty Finance, which he had invested at least $75M into before having his assets locked.

Sun is now going public with his frustrations, alleging that the team is yanking around their investors while serving as "the antithesis of decentralization."

Per Sun:

Enjoying this article?

Subscribe to Bankless or sign in

Every action taken by the WLFI team—from extracting fees from users, secretly implanting backdoors to control user assets, freezing investor funds without disclosure or due process, treating the crypto community as a personal ATM—is unjust and has never been authorized through any fair, transparent, good-faith community governance process.

These are accusations that would be shocking for just about any project, let alone one founded by... the sitting U.S. president – the self-proclaimed Crypto President at that.

All the while, other WLFI grumblings have been impossible to avoid this week, including concerns that the Dolomite DEX, run by World Liberty's CTO, is taking unacceptable bad debt risk on massive World Liberty loans taken against the project's WLFI tokens.

While World Liberty's official X account accused Sun of "playing the victim," Sun's post has seemed to signal a public vibe shift against the project and, perhaps, Trump's role in the industry itself.

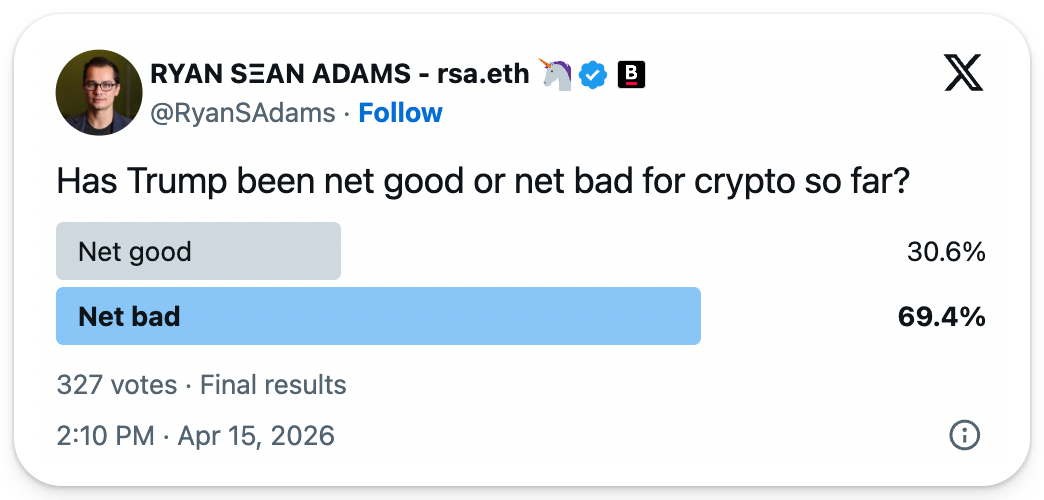

Ryan's X poll this week asking whether Trump's presence in the crypto space had been a net positive or negative saw 7 in 10 respondents choosing the latter.

And while recent World Liberty moves may prompt some retail investors to think twice before putting money into the Trump crypto machine, crypto industry leaders scarred by the Biden Administration's lack of engagement with the industry have no clear reason to distance themselves.

This all sets up the looming scenario – one plenty inside the space have openly wondered about for a while now – where Democrats wage a renewed vendetta against the industry (whenever they take back power) as a proxy war on the President's businesses.

Last month, Bankless mapped out what appears poised to be a brutal Midterm election cycle for the Republicans, with Democrats currently favored to take control of the House and Senate – and, more critically, the committees key to future crypto legislation.

Democratic leaders have already tried to probe Trump's crypto businesses as the minority. If they take power, investigations into conflicts of interest and particular foreign deals tied to these efforts are almost certain.

How much further than that they go is likely going to have a lot to do with how much the "War on Crypto" messaging resonates with voters. But if even the crypto community is having a tough time defending the President's actions inside the industry, we might be in trouble.

Emerging markets provide some of the best yield on Earth. Opportunities shouldn't be constrained by geography or capital. Brix provides access to real yield, not made-up onchain mechanisms. Let the Yield Flow.