Subscribe to Bankless or sign in

Dear Bankless Nation,

The bear market is wreaking havoc throughout crypto.

Prices are down bad. Major industry players are immolating at its altar. Market sentiment on Crypto Twitter feels like getting shock therapy at a funeral.

Terra and Celsius were exposed and disemboweled by market forces in a matter of days. Now, Three Arrows Capital (3AC) is rumored to be facing insolvency.

It’s rough out there. The bad actors are getting flushed out. That also means it’s now open season for DeFi — no one is safe.

Crypto continues a rapid slalom descent, macro-economic sirens ring louder daily, and multi-billion dollar crypto businesses devolve from Twitter whistleblower to insolvency in less than a Thanos snap.

With everything blowing up in our faces, you might be asking…“Is DeFi Ded?”

Ben Giove puts his stethoscope on to find out.

— Bankless

What This Bear Market Means for DeFi

The Current State of DeFi

Let’s take a look at some on-chain performance indicators to assess where DeFi stands today, and to what extent liquidity and activity have contracted since the bear market.

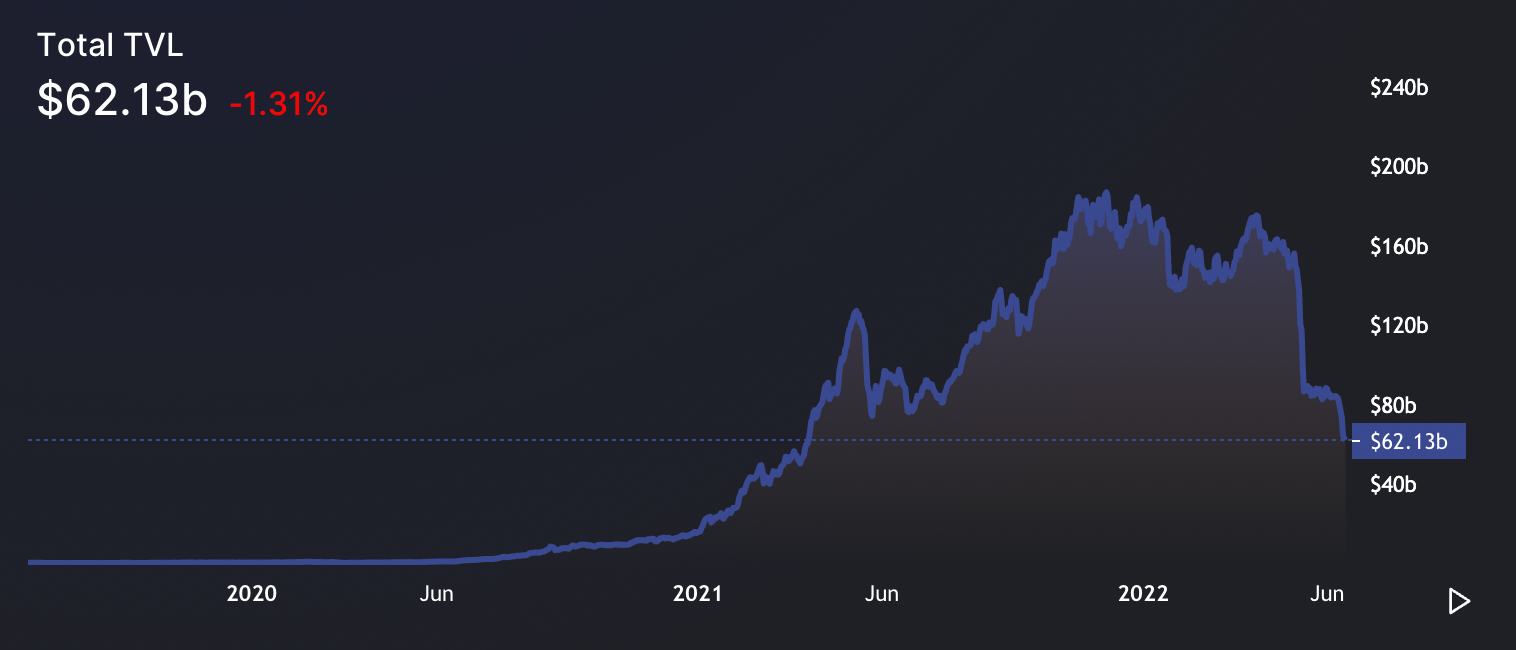

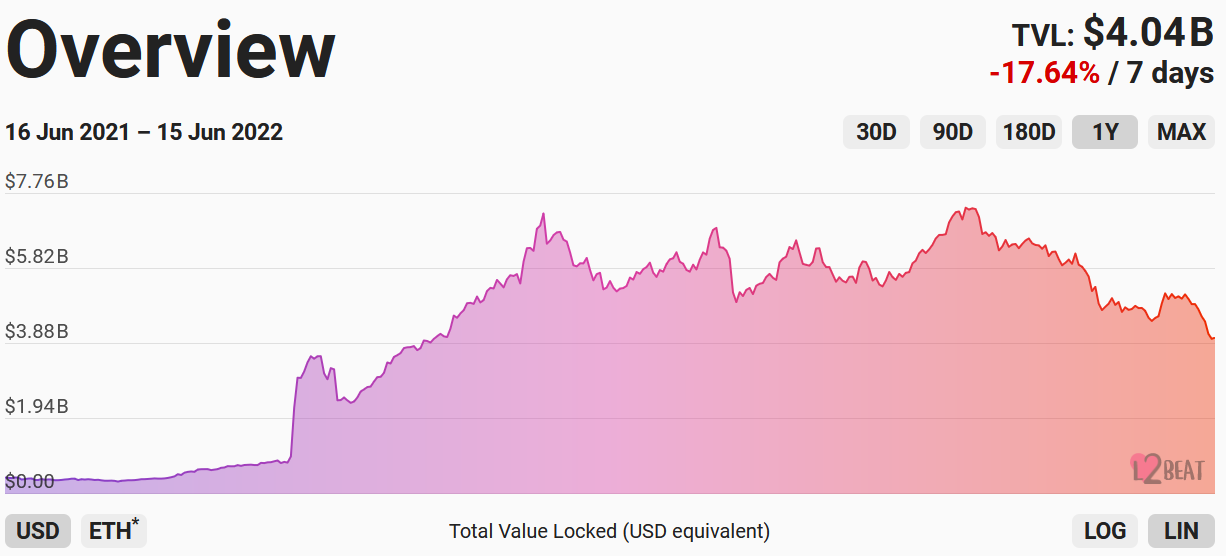

Total Value Locked (TVL)

The total TVL across multi-chain DeFi sits at $62.59B. This represents a 66.5% decrease from the all-time high of $186.8B reached in December 2021. This drawdown has been driven by declines in widely integrated assets such as ETH and wBTC, as well as capital outflows that are likely attributable to the compression of yields.

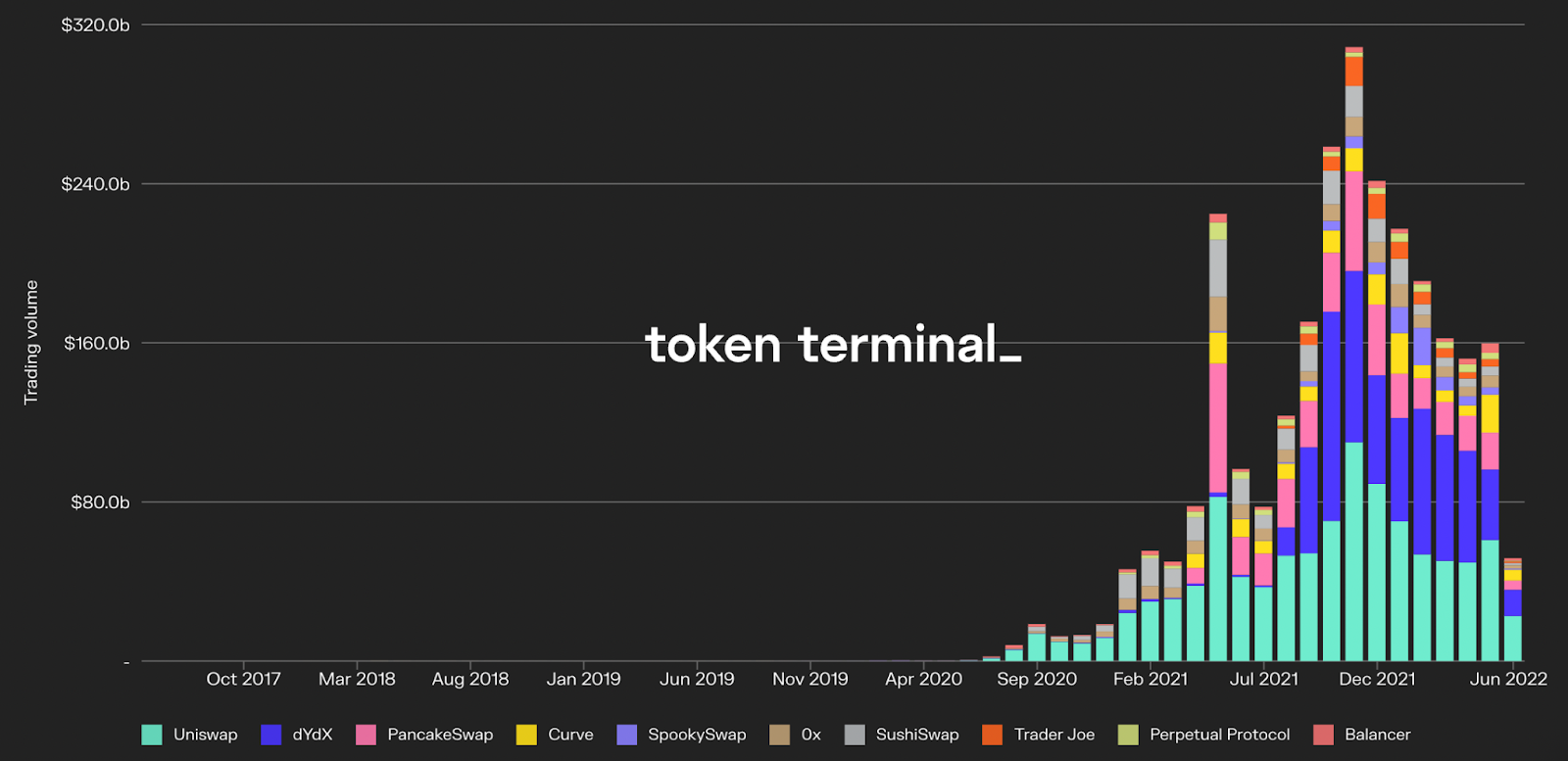

DEX Volumes

Monthly DEX volume sits well below its November 21, 2021 peak at $308.6B. Volumes for June 2022 are currently on pace to clock in at $103.3B. This would represent a 66.2% decline across the 10 platform sample set. As trading activity and price appreciation are highly correlated, this downward trend is likely attributable to the market weakness of the past several months.

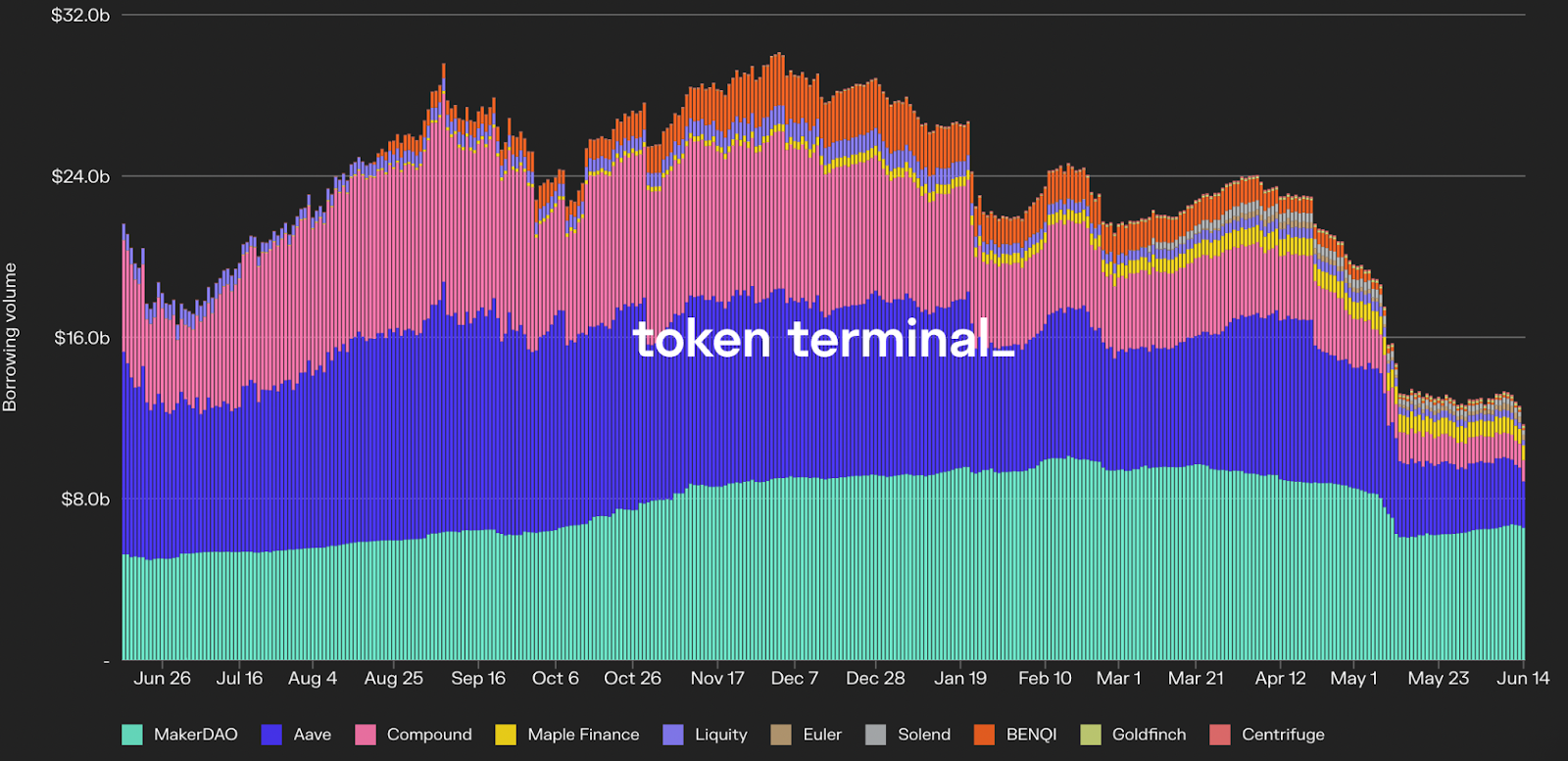

Borrow Volume

Borrow volume — which measures the value of outstanding debt on lending protocols — currently sits at $5.1B. This represents a 75.3% decrease from its peak of $21.1B in December 2021. Decreased demand for loan leverage is a direct factor of the current bearish climate.

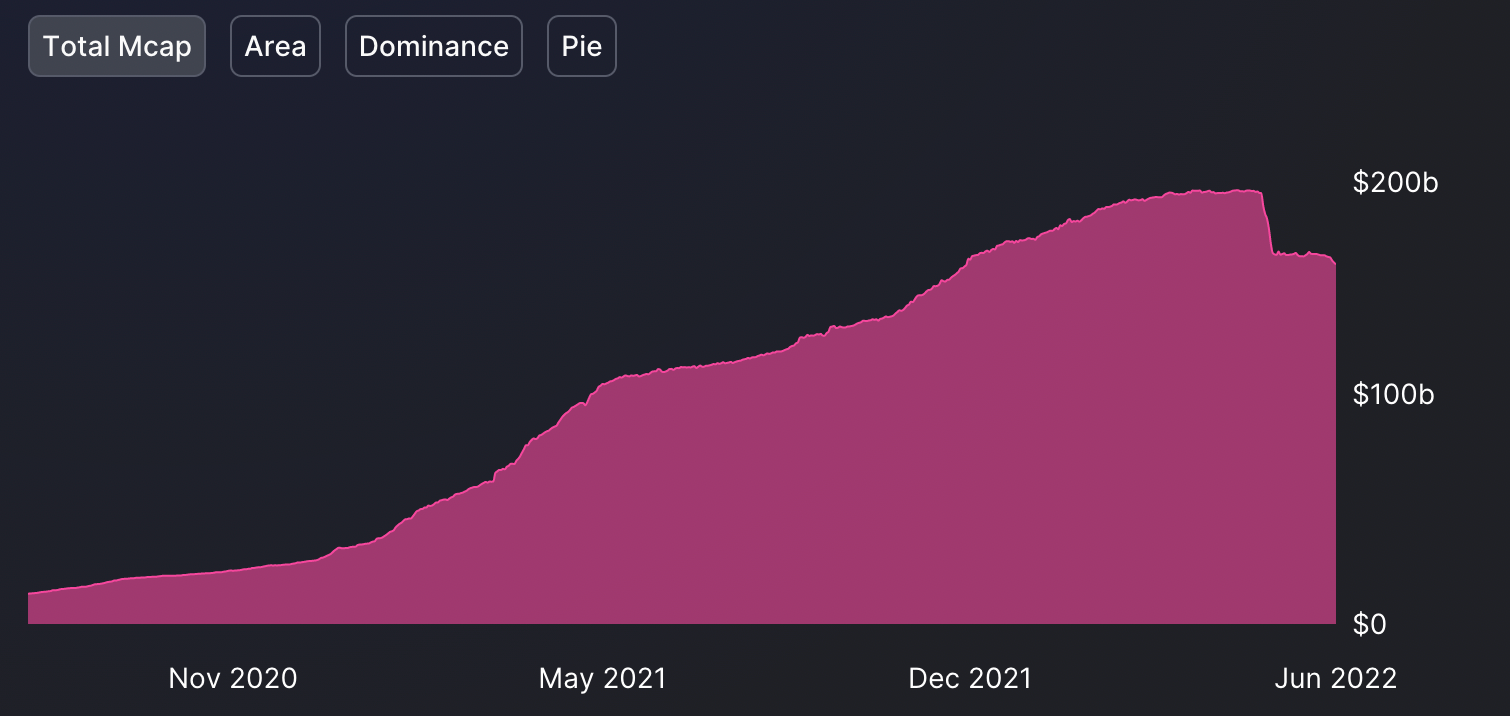

Stablecoin Supply

The market capitalization (outstanding supply) of stablecoins is currently $156.7 billion. This is a 17.1% decrease from its peak of $188.9 billion in May 2021. This decline coincides with the collapse of UST, which at its peak had a market cap of more than $18.7B. This led to contractions in the supply of other stablecoins — such as USDT, BUSD, and DAI — as holders redeemed assets amidst the panic.

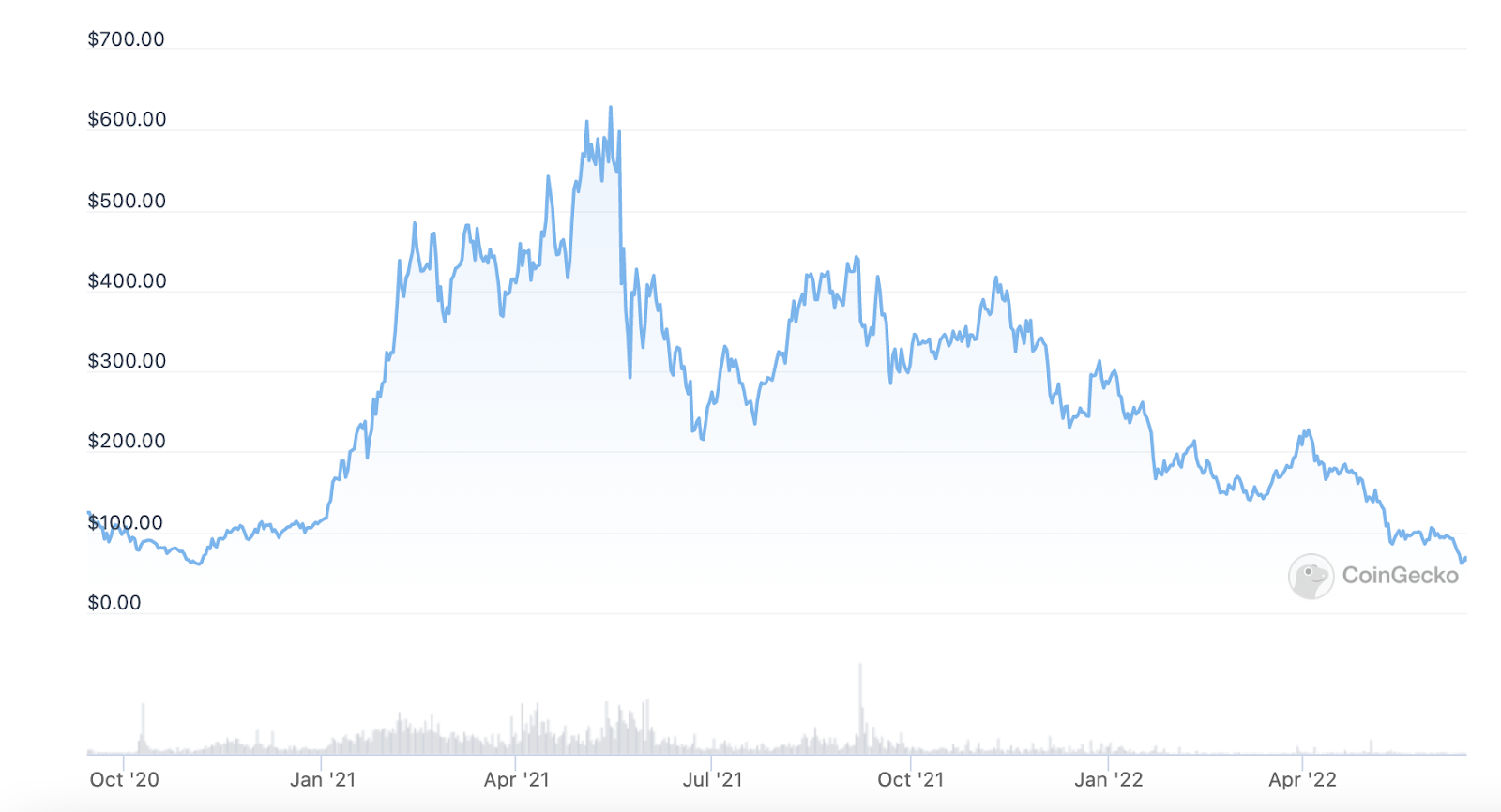

Token Prices

DeFi tokens have cratered from the all-time highs of Spring 2021. DPI — the largest DeFi index by assets under management (AUM) — has fallen 90.3% from its peak of $656.49. It currently trades at $63.45.

Beyond these broad market weaknesses, the decline in DPI — which holds a basket of fourteen DeFi tokens — has been exacerbated by inflationary token rewards. Many DPI constituents offer active liquidity mining programs, incentives that are far less appealing in current market conditions.

Takeaways:

Capital is leaving the ecosystem. Users are trading less and borrowing less. Stablecoins are being redeemed for horrible, filthy fiat by the billions.

This is all coming as DeFi tokens continue to bleed market value, while the global economy enters its very own bigger, badder bear.

Spoiler alert: DeFi is in the midst of a significant contractionary period.

DeFi’s Self-Inflicted Struggles

Now that we have a sense of the extent of DeFi’s first historically significant contraction period, we can dive into some of the root causes of declining prices and the correlated slowdown in on-chain activity.

Reflexivity of Yields

DeFi yields are highly reflexive. This is due to the correlation between price action and on-chain activity.

As the broader crypto market rallied at the end of 2020 and onwards, protocol usage, liquidity, and leverage soared along with it. This increased usage also led to higher yields, as liquidity providers earned more swap fees, deposit rates on lending markets rose, and token-denominated incentives increased in value. The increase in yields led to more capital flowing into DeFi. Degens and farmers rejoiced in taking advantage of APRs that routinely reached upwards of four or five figures.

Some people called it a utopian virtuous cycle. Others just called it greed.

The thing is: reflexivity cuts both ways.

As prices have fallen, so has on-chain activity. This has caused yields to fall in concert and has driven the outflow of liquidity. Deploying capital in DeFi becomes less attractive when returns are lower, and right now the returns are looking straight up ugly.

The yield compression is real. Deposit rates for stablecoins on Compound and  Aave (between 0.7-1.7%) are currently lower than the yields on t-bills, which is the shortest duration US treasury bond.

Aave (between 0.7-1.7%) are currently lower than the yields on t-bills, which is the shortest duration US treasury bond.

Even if the federal government can offer better deals than DeFi, users may feel that they are not being properly compensated for the considerable risk that comes with engaging with the frontier economy of decentralized finance.

Over-reliance on Liquidity Mining

DeFi’s contraction in activity and price has been exacerbated by an industry-wide overreliance on liquidity mining. Degens may think of liquidity mining as the gamification of finance and a big win for DeFi, but the practice has enshrined a system of monetary incentives that has stimulated unsustainable growth and will need to be improved.

Popularized by Compound in July 2020, LM incentive programs powered the first wave of DeFi adoption by providing protocols with an incredibly effective tool to quickly bootstrap usage and growth through subsidizing yields with their native token.

Despite the effectiveness of liquidity mining as a short-term growth hack, it has several important drawbacks. For starters, incentive programs have proven to be a magnet for mercenary capital, as liquidity often flows out of a protocol or DEX pool as soon as rewards begin to subside or yields compress.

In addition, liquidity mining places downward pressure on the price of the reward token — almost always the protocol's own governance token — as farmers realize their yield through sale of this asset.

Enjoying this article?

Subscribe to Bankless or sign in

In turn, this accelerates the decapitalization of DAO treasuries as protocols often allocate a substantial portion of their native token supply to these rewards programs. This decreases a protocol’s funding runway, and with it goes its resiliency against adverse macroeconomic conditions — the likes of which we find ourselves right now.

Protocol Blowups and Exploits

As the bear market progresses its biblical carnage, numerous events have damaged trust and highlighted key risks inherent to DeFi.

The most prominent of all thus far has been the implosion of Terra.

As you might have heard, both Terra’s UST stablecoin and its seigniorage token LUNA collapsed in May. UST de-pegged. LUNA hyper-inflated. The result was a 99.9% value collapse within just a few days. Based on the peak market cap of each token, this represented a combined wipeout of ~$59.8B in investor value. That’s just about the GDP of New Zealand, vanishing like a Kiwi bird in the mountain mist.

The UST death spiral contagion spread to other Terra protocols like Anchor, a money market that paid a fixed ~20% rate on UST deposits that were billed to users as a “savings account.” The protocol was one of the largest in all of DeFi, at its peak accumulating more than $17.15 billion in TVL.

Along with protocol implosions, DeFi has also been ravaged by hacks since before the bear market even began. More than $1.44B of user funds have been lost across 20 exploits in 2022 alone, which already exceeds all of the value lost in 2021. The frequency and magnitude of these attacks has likely contributed to the sharp decrease in on-chain activity, as the prospect of losing funds, coupled with the compression in yields, has made the risk-reward profile of deploying capital on-chain less attractive.

Both the destruction of UST, as well as the billions in stolen funds, have sown a deep distrust among users in regards to DeFi protocol design and security.

The Catalyst For a DeFi Revival

Now that we understand why DeFi prices and activity have contracted, let’s explore some of the potential catalysts for reviving the sector's growth model.

1. Scalability Unlocks

A primary reason as to why DeFi adoption has been limited to a small pool of eager degens thus far comes down to — that’s right — scalability constraints.

Despite respite, gas fees on  Ethereum remain so high that they price out a large portion of potential users. This not only restricts the types of applications that can be built but also encourages poor risk and position management on those that are built.

Ethereum remain so high that they price out a large portion of potential users. This not only restricts the types of applications that can be built but also encourages poor risk and position management on those that are built.

For example: to save on gas costs, users handling smaller amounts of funds are forced to concentrate capital across fewer protocols. This means they’re unable to adjust positions as they’d like, and maybe not even at all. Imagine playing chess but having half as many moves as your opponent. That’s your handicap on CeFi platforms.

While scalability issues are not just limited to congestion on Ethereum, it is on Ethereum that solutions are being rolled out as we speak via solutions like optimistic and zk-Rollups. Although the technology is still nascent, these Layer 2 (L2) networks have begun to see meaningful adoption and transaction volume. ![]() Arbitrum and

Arbitrum and ![]() Optimism have managed to attract a combined $1.2B in TVL, while dYdX — built using Starkware’s StarkEx — is now the largest perpetual DEX by volume.

Optimism have managed to attract a combined $1.2B in TVL, while dYdX — built using Starkware’s StarkEx — is now the largest perpetual DEX by volume.

By providing users with cheaper transaction fees and near-instant semi-confirmations, L2s not only dramatically improve user experience and unbound platforms but will enable en masse onboarding a new wave of users into DeFi.

L2s also unlock a new design space for developers. Many of the most popular applications on these rollups today are ones that were impractical to build on L1 — such as derivatives protocols, for example. Along with dYdX, other perpetual exchanges like  GMX and Perpetual Protocol, along with options protocols

GMX and Perpetual Protocol, along with options protocols ![]() Lyra* and Dopex, have emerged as some of the most trafficked platforms on their respective networks.

Lyra* and Dopex, have emerged as some of the most trafficked platforms on their respective networks.

As these scalability solutions gain traction, mindshare, and liquidity, we should continue to see new, novel applications be built that weren’t possible to create on L1 or within the confines of TradFi rails.

So, if you thought degens and liquidity mining was wild, wait ‘til you meet the degen regens and their definition of ‘financial instrument.’

2. Very Real Real World Adoption

Another factor that will help revive DeFi is our ever-elusive old friend “real-world adoption.”

Although there are billions locked in DeFi today, much of this has come from a small group of whales and retail users. Due to a lack of easy onboarding and regulatory concerns, there has been little adoption and usage of DeFi outside of yield farming from this select cohort.

There have now emerged myriad routes through which DeFi can be utilized by a more diverse group of market participants, which in turn fuels growth and injects new liquidity into the ecosystem. The road to bringing in tens of trillions in capital is getting paved.

For example: protocols such as Maple Finance, Clearpool, and TrueFi provide a means for institutions to use DeFi to obtain undercollateralized loans in a compliant manner, allowing them to benefit from the decreased transaction costs and increased efficiency that comes with operating on-chain. These lending protocols have exploded in popularity, with Maple recently crossing $1.5 billion in loan originations.

While these loans have already been largely extended to CeFi entities like market makers and hedge funds, the same infrastructure can eventually be leveraged by traditional financial institutions that hold far more capital at their disposal.

Products like Aave ARC, which offers whitelisted KYC’d pools, provide another venue in which TradFi institutions will want to dip their decrepit, gouty toes into the waters of the on-chain economy — and then the real battle for DeFi will begin.

Along with institutions, we are also seeing early signs of real-world businesses leveraging DeFi. Goldfinch, a decentralized credit protocol, has originated more than $102.2 million in loans to businesses operating in markets like Nigeria, Southeast Asia, and Mexico.

This represents another avenue in which DeFi can grow its user base, bring in new capital and demonstrate its value proposition by actually providing financing in the real-world.

Conclusion

The rapid and consecutive combustion of UST (a stablecoin), Terra (UST’s Layer 1), Celsius (a CeFi bank), and Three Arrows Capital (Terra’s VC) was by no means spontaneous. The contagion spread fast from the sickly product layer to its parent organization within days of discovery and with fatal consequences. COVID would be proud.

Ultimately, none of these projects were built on Ethereum, and none of them are DeFi platforms. In fact, the value proposition of the fully transparent and open financial system that DeFi provides has never been clearer in their wake.

Kind-of-decentralized is NGMI. That acronym rings a little different now.

So what’s next? Scalability solutions like L2s mean DeFi will soon have the bandwidth to onboard a new generation of users. The build market means developers are free to build edge-case prototypes instead of rushing for quick win copycats. DeFi lenders are intersecting with meatspace businesses to get this jack out of its box.

This lays out the path for trillions in new capital to flush into the ecosystem and propel it forward.

Yes, DeFi may be down bad.

But it is certainly not ded.

In fact, DeFi doing just fine.

Action steps

- 💸Read our explainer: ‘How to Get Started in DeFi’ 💸

- 👂Catch up on Ryan and David’s Emergency Bear Market Update show