Subscribe to Bankless or sign in

Yesterday, Strategy disclosed it sold 3,588 BTC for roughly $216 million between June 29th and July 5th.

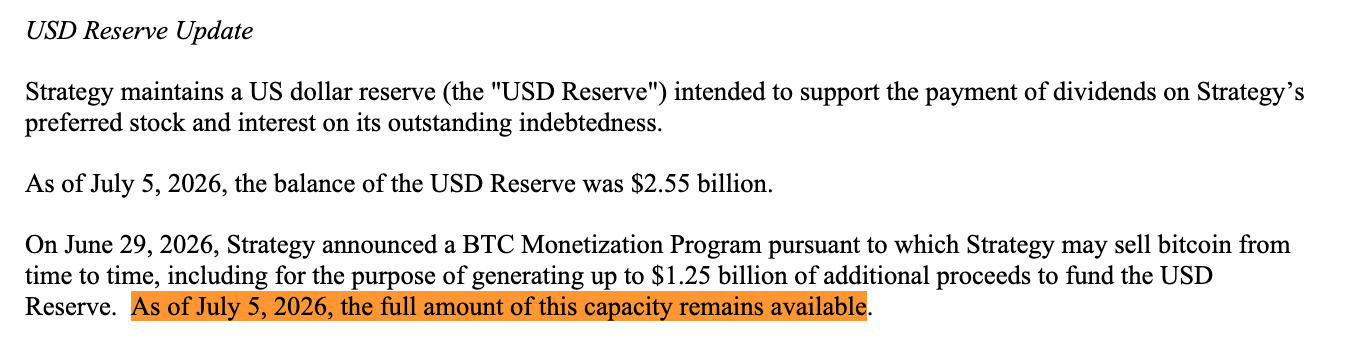

The proceeds funded STRC distributions and refilled the portion of the USD Reserve used to make them. Despite the sale, Strategy said its full $1.25 billion of reserve-building capacity remained available.

So a $216 million sale to replenish the reserve did not count against the billion-plus allotted to build it. Technically there's a difference: replenishing versus building. But both sales feed the same reserve, for the same purpose, classified differently.

Put it this way: the BTC Monetization Program never capped total ![]() Bitcoin sales at $1.25 billion. It capped one bucket: selling BTC to build the USD Reserve. The program lets Strategy sell BTC for other purposes too, which is what we just witnessed.

Bitcoin sales at $1.25 billion. It capped one bucket: selling BTC to build the USD Reserve. The program lets Strategy sell BTC for other purposes too, which is what we just witnessed.

The Three Buckets

On June 29th, after weeks of pressure on MSTR and STRC, Strategy introduced the BTC Monetization Program as part of its larger Digital Credit Capital Framework. The program lets Strategy sell Bitcoin for three primary purposes:

- Build the reserve — Sell up to $1.25 billion of BTC for the USD Reserve.

- Cover the preferreds — Sell BTC to pay the fixed dividends and interest Strategy owes on its preferred shares and debt, or to replenish the reserve afterward, when management decides selling BTC beats issuing common stock.

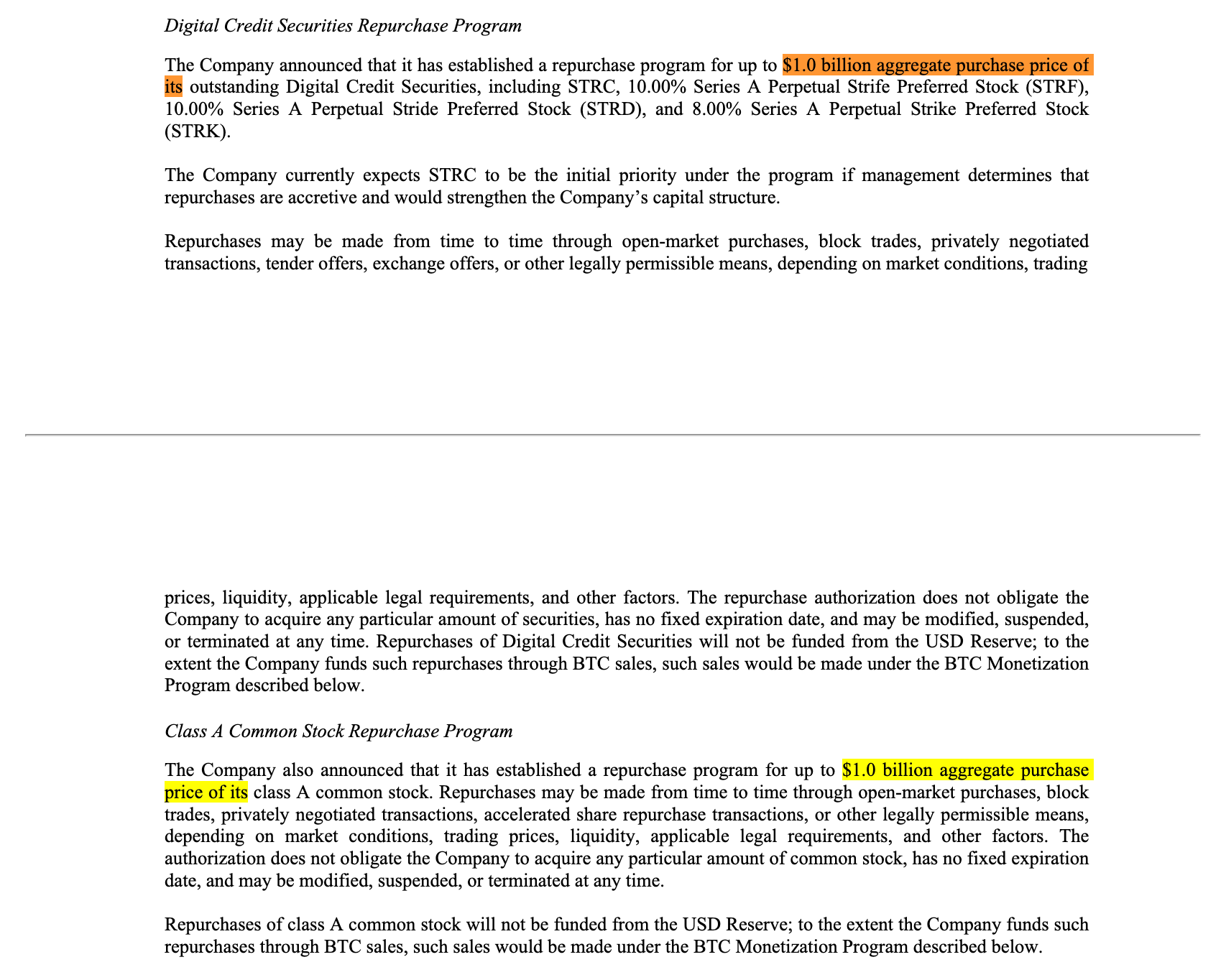

- Fund buybacks — Sell BTC to repurchase its preferred shares or MSTR common stock, up to $1 billion of each, with BTC sales potentially covering related taxes, fees, and expenses.

Only the first bucket carries the widely circulated $1.25 billion figure. The third adds another $2 billion across the preferred and common repurchase programs.

So, the capped pieces alone already contemplate more than $3 billion of BTC monetization, and that excludes the dividend/interest/replenishment bucket, which carries no disclosed cap.

Building vs. Replenishing

This is where the distinction gets thin.

The USD Reserve exists to pay those preferred dividends and interest obligations. It cannot fund stock buybacks under current policy.

As of June 28th, it held $2.55 billion, enough to cover roughly 17 months of the $1.76 billion Strategy owes each year. The Board set a 12-month coverage floor unless it authorizes lower.

That is why the line between building and replenishing deserves scrutiny.

- Sell Bitcoin to add cash before dividends are paid: building.

- Use the reserve to pay dividends, then sell Bitcoin to refill it: replenishing.

The program treats these as different categories while they do the same thing: turn BTC into cash to cover preferred dividends and interest.

The fine print was already disclosed, but yesterday's sale showed how convenient the distinction is. Strategy sold $216 million of BTC, spent it on distributions and replenishment, and still reported full reserve-building capacity at $1.25 billion.

Enjoying this article?

Subscribe to Bankless or sign in

We must all now learn Strategy-speak. "Build" and "replenish" are just accounting details, but they determine whether a BTC sale reduces the headline capacity.

Strategy has sold 3,588 $BTC for $216 million to fund dividends on our Digital Credit securities. As of 7/5/2026, we hodl ₿843,775 in our BTC Reserves and $2.55 billion in our USD Reserves. https://t.co/Cssgz29Psj

— Michael Saylor (@saylor) July 6, 2026

From Accumulation to Active Management

In the June 29th announcement, Michael Saylor said the framework reflects a need for "liquidity, discipline, and active capital management." CEO Phong Le put it plainly: Strategy is "evolving from one-way capital issuance to active capital management."

Strategy has effectively become an actively managed hedge fund, as Castle Island's Matt Walsh and Jeff Dorman explained when they stopped by the podcast last week.

The old Strategy story was simple: sell MSTR equity, buy Bitcoin, and hand investors levered BTC exposure. The new one isn't: Strategy is now buying and selling pieces of its own capital structure to manage pressure between the common stock, the preferreds, the reserve, and Bitcoin itself.

That dynamic creates conflicts, as Walsh and Dorman note. Selling common equity supports preferred dividends but pushes down the premium MSTR trades at over the Bitcoin it holds. Selling Bitcoin extends the cash runway but further weakens the "never sell" narrative. Supporting preferreds protects confidence but drains cash. Cutting preferred dividends preserves liquidity but could crater the preferreds themselves.

The reserve loophole is one expression of that shift. Bitcoin is now a balance-sheet lever to keep the preferred stack functioning, not an asset Strategy accumulates.

.@jdorman81 on @Strategy's new $MSTR playbook:

— Bankless (@Bankless) July 1, 2026

“There's no trigger for it to go bankrupt here.”

“The problem... is simply that each part of the cap structure is in a war with the other parts.”

“Everything that is good for one part is gonna be negative for other parts.”… https://t.co/vUpnT0PFWF pic.twitter.com/aIRryEdtJj

What We're Left With

Investors must now underwrite Saylor's ability to run a machine where every lever helps one part of the capital structure while threatening another.

That is the real takeaway from the July 6 filing. Strategy is not out of options. It may have more than the headline suggests. The $1.25 billion figure signals that BTC preservation remains the priority only if investors mistake it for a total ceiling. Don't make that mistake.

Strategy is now an institution the market has to interpret.

Every phrase matters now: build, replenish, issue, repurchase, defend. Like Fed-watchers parsing every comma, we must parse each term for what it implies about future BTC sales.

With the Program, Strategy bought itself flexibility, but the underlying tension remains. This is no longer a clean levered Bitcoin trade. It is a bet on active capital management: whether Strategy can keep selling, refilling, issuing, repurchasing, and defending pieces of its capital structure without one breaking the others.

Personally, it's not a bet I'd like to make.