Subscribe to Bankless or sign in

How cool would it be to have Bankless in video format? That’s where I want to go next. But I need your help! If you want the Bankless program in video give 1 DAI & let’s make it happen!

Dear Bankless Nation,

I had a conversation recently with JJ a VC & the author of today’s piece.

We had the same baffling question—why are all the Fintech VC’s missing DeFi?

“Maybe” JJ said…“maybe it’s because they’re making the same assumption. They’re assuming SWIFT continues to be the financial router for the world.”

But that’s not what we see.

We see  Ethereum addresses replacing SWIFT codes and bank accounts.

Ethereum addresses replacing SWIFT codes and bank accounts.

We see DeFi as the settlement platform for the next wave for fintech.

We see bankless protocols replacing the banker infrastructure.

I asked him to write this all down for us and he turned it into this incredible article.

Send this one to your favorite VC.

Or…maybe just front-run the VCs & let them figure it out later.

Either way—read this now.

FinTech on Ethereum.

It’s happening.

🚀

- RSA

🙏Sponsor: Aave—earn high yields on deposits & borrow at the best possible rate!

THURSDAY THOUGHT

Technology Cycles & the DeFi VC Paradox

Guest Post: Jonathan Joseph (JJ), founder of Smart Money

One of the fun aspects of working in DeFi is that feeling that you’re in on a really big secret.

Peter Thiel is always on the lookout for billion-dollar ideas hiding in plain sight. Well, DeFi is a trillion-dollar idea hiding in plain sight. Maybe even a few hundred trillion depending on how you want to measure it.

DeFi (Decentralized Financial Services on Ethereum) is a programmable fintech platform. Ethereum’s smart contracting capabilities and token standards combine to enable an incredibly powerful (and open) set of developer tools for building new financial technologies.

But DeFi is not “crypto”. It may or may not involve cryptocurrencies at all, which is part of what leads to a lot of confusion. As a result, DeFi remains almost completely off the radar for the traditional fintech industry and the venture capitalists (VC) who invest in those companies.

If DeFi is a massive paradigm shift for financial services and fintech, how is it such a well-kept secret? Platform shifts are typically catnip for the venture capital asset class, and yet there’s a notable dearth of early-stage capital.

What explains this paradox?

Platform Shifts And A Brief History Of Venture Capital

The venture asset class came about as risky early-stage ventures without reliable cash flows typically couldn’t access capital through traditional banking. This created a new and highly specialized form of finance, understood to be more of an art than a science. This new form of financing essentially funded the research and development of new technologies with the hope of earning outsized returns for its investors.

The earliest venture capital firm, American Research and Development Corporation, literally had R&D in their firm’s name. Assumption of this degree of risk is what justified a 10-year closed-end, illiquid investment vehicle.

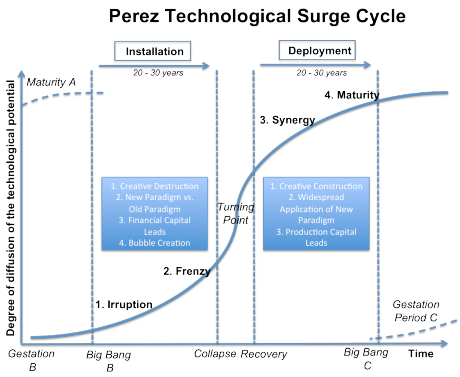

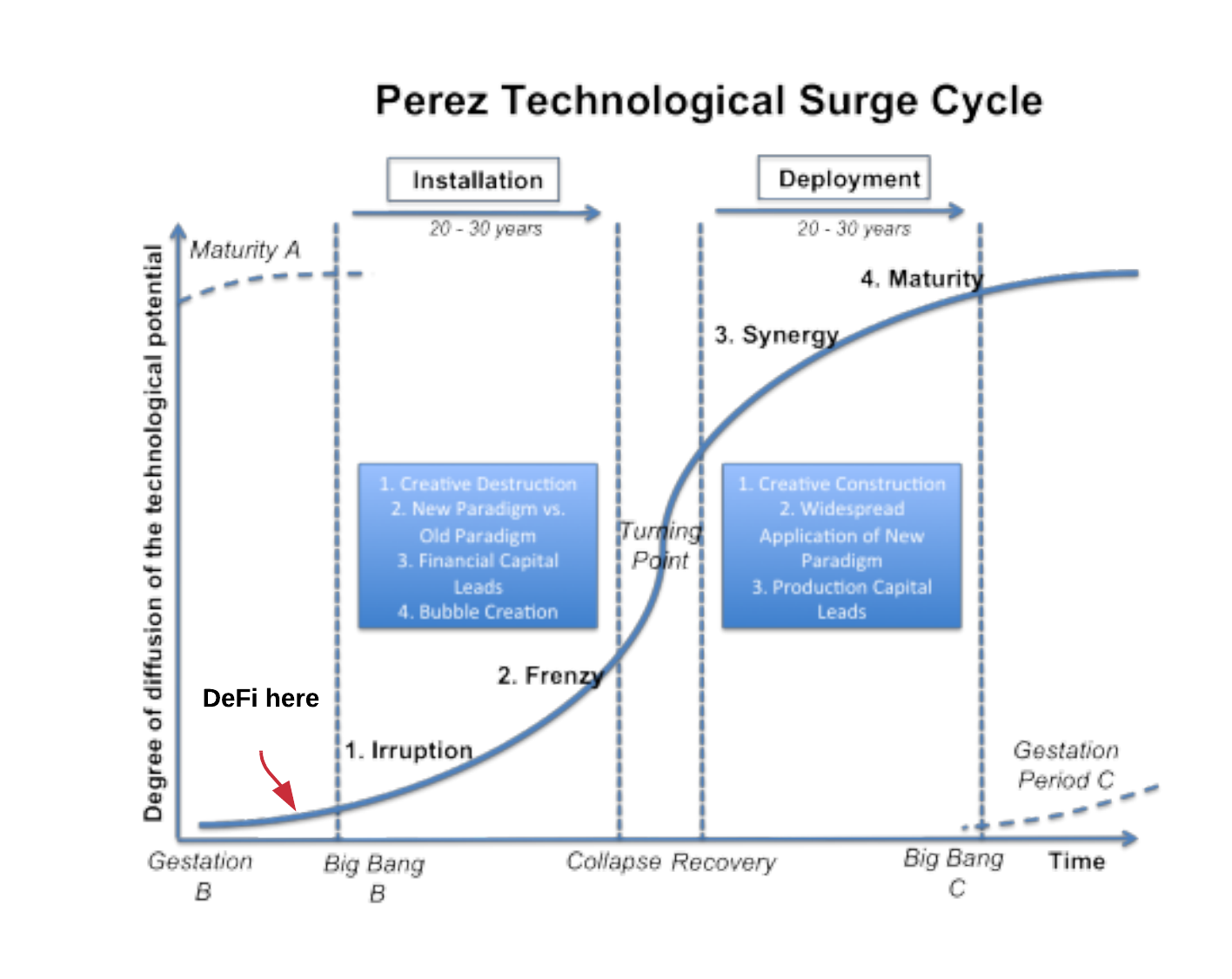

Key to understanding the pursuit of outsized returns is understanding early-stage technology markets and the timing and cycles of technology platforms. Carlota Perez’ work here on Surge Cycles is canonical.

In order to achieve outsized returns, it’s rational to allocate capital more heavily towards technology platforms at the early stages of their S curve.

But is that what we see in practice?

A Dearth of Early Stage Blockchain VC

Those that know early-stage technology also know that history doesn’t repeat itself, but it does rhyme. The parallels between the dot com bubble in 2001 and the ICO bubble in 2017 aren’t hard to spot.

Just as it was for Web startups post-dot com crash, crypto startups broadly find themselves in the throes of the trough of disillusionment three years after the ICO bubble burst - another reference to a well-known technology cycle.

Even before COVID, early-stage blockchain venture deal volume and dollars had been falling off a cliff. From a recent analysis by Joel John (Outlier Ventures):

“To put it in simple terms - if you are in the pre-series B levels, there is only about $50 million that gets deployed on the average month.”

“In fact, If fewer seed-stage companies are backed, we will not have a healthy crop of growth-stage firms 18 to 24 months from now. The power laws at play dictate that we have a large enough crop of firms at the early stages to continue optimising for the late stages.”

The above funding levels are inclusive of all “blockchain” funding. DeFi remains one sector within blockchain/crypto, and a sector that some blockchain VCs are actively betting against (via “ETH killers”).

Per Brooke Pollack’s (Hutt Capital) recent estimate, the current $1B-$1.5B in dry powder for blockchain/crypto VCs represents ~0.5% of global VC dry powder.

🧠 Note: Dry powder is a commonly used term in the VC and startup world. It refers to the cash reserves (or highly liquid assets) kept on hand by a company or venture capital fund.

Separate out “early stage” and “DeFi” from aggregate blockchain venture capital and the capital available to DeFi startups amounts to a rounding error. While you would expect the next big thing to start out looking like a toy, this takes that adage to a new extreme.

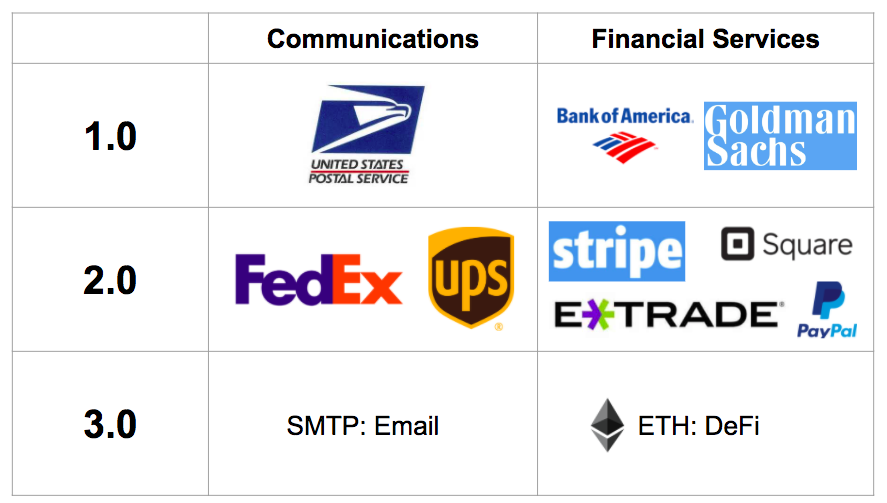

SWIFT, Stripe and Plaid—Platforming the Existing Fintech Stack

Even more curious, the current low watermark in crypto VC funding runs concurrent to a fintech funding boom, even if it may have peaked in 2018. One of the biggest drivers of this fintech boom cycle has been using developer tools to enable platform-like dynamics.

Enjoying this article?

Subscribe to Bankless or sign in

But every assumption about fintech today assumes SWIFT’s continuing role as the dominant global financial router. It’s not only the current global standard for international bank messaging, but also for enforcing sanctions through denial of access to the SWIFT network.

Technically speaking, SWIFT is a protocol. Just not a very useful one for the modern era given that SWIFT was created in 1973. SWIFT assigns codes to member banks and transactions and routes messaging among the member banks using those codes.

SWIFT’s critical flaw is that it’s just a messaging standard, it does not actually facilitate the transfer of value. Because of those fundamental technical limitations, everything built on the existing fintech stack is subject to those design limitations, flawed from the start.

This also helps explain the dramatic success of companies like Stripe and Plaid. Their developer tools made it easier to build fintech products, demonstrating the value of reducing the technical debt associated with building products on the SWIFT architecture.

But in the grand scheme of things, these technologies are incremental improvements, irreparably hamstrung by the underlying technical debt.

For example, critics fairly point out that some of Plaid’s bank connections use screen scraping, indicative of substantial security holes. And per Plaid’s own data, this labored approach results in somewhere between 2%-5% of requested bank authentications failing, a failure rate which would typically be unacceptable for software.

Just taking most of the friction out of accepting payments and accessing financial data was enough to create massive enterprise value and a sustained wave of fintech innovation. But this innovation is still fundamentally and structurally limited to the application layer of finance.

DeFi Is A Programmable Fintech Platform

Without getting too far in the weeds in this post, DeFi is an open source Fintech platform that is unburdened by legacy technical debt and built on transparent, sound economics and monetary policy. In the DeFi economy, the Ethereum blockchain is the global settlement layer and ETH is the base layer currency, or “M0”. Unlike the incumbent SWIFT architecture, every layer of the stack is programmable including the base currency itself.

Beyond programmability, DeFi’s secret sauce is its combination of standardization and composability. And the impact will be profound.

As Dmitriy Berenzon (Bollinger Investment Group) noted in his recent post on Constant Function Market Makers, DeFi has found it’s “zero to one” innovation in liquidity protocols.

This substantial innovation in liquidity removes the friction (middlemen, relationships, and paperwork) that clog current capital markets, enabling a frictionless flow of liquidity that modern global financial markets need.

“Earnings don't move the overall market; it's the Federal Reserve Board... focus on the central banks, and focus on the movement of liquidity... most people in the market are looking for earnings and conventional measures. It's liquidity that moves markets.”

-- Stanley Druckenmiller

Protocols, smart contracts, and code libraries are emerging for every type of financial instrument (and some that weren’t even possible before) on top of continued innovation in trading and market-making via smart contracts. Because DeFi is both standardized and composable, the design space for finance and financial services becomes exponentially greater. Any type of transaction or financial instrument that is sound becomes possible for anyone in the world with an internet connection.

Once the DeFi technology stack is mature and the DeFi economy has grown to a sufficient scale, every product or company built on the legacy fintech stack will find it extremely difficult to compete with DeFi products. This is as surely true as it was for the best horse and buggy companies at the invention of the automobile. DeFi technology is not mature enough to fulfill that promise yet, but it’s making progress towards that end faster than anyone realizes.

Among those who still “don’t realize” are traditional fintech incumbents and the VCs who are funding them. Broadly, they still believe that the existing tech stack is well entrenched and don’t recognize DeFi as a viable threat.

How DeFi Breaks The Existing Paradigm

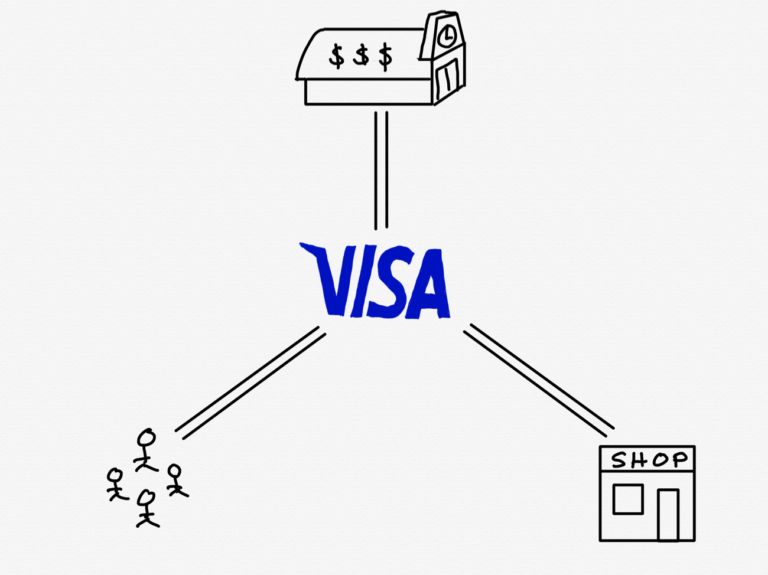

Ben Thompson’s analysis of Visa’s acquisition of Plaid breaks down what appears to be that very entrenched network effect for the legacy stack. In it, he explains that Visa sits in the middle of a powerful multi-sided network among banks, merchants, and consumers.

“Once a job is done — and credit cards do their jobs very well — it takes a 10x improvement to get users to switch, and, in a three-sided network, that 10x is 10^3.”

Ironically in the process of explaining the entrenched network effects, this ends up highlighting why DeFi will be so disruptive.

In the DeFi economy, Ethereum addresses replace both SWIFT codes and bank accounts. The DeFi stack re-routes the value that traditionally accrued to the Visa network and banks back to the merchants and consumers.

The best part? Merchants and consumers get better banking and financial services. Banks become unnecessary middlemen. Hence why we’re going Bankless.

That’s just the sort of 1,000x improvement that can break even seemingly well-entrenched network effects.

Adoption of DeFi Infrastructure Is Happening Now

No group has been more vocal about the limitations of the SWIFT architecture than the world’s central banks, not typically champions of innovation. One day in the future, the central banks will issue their currencies digitally to compete with this liquidity.

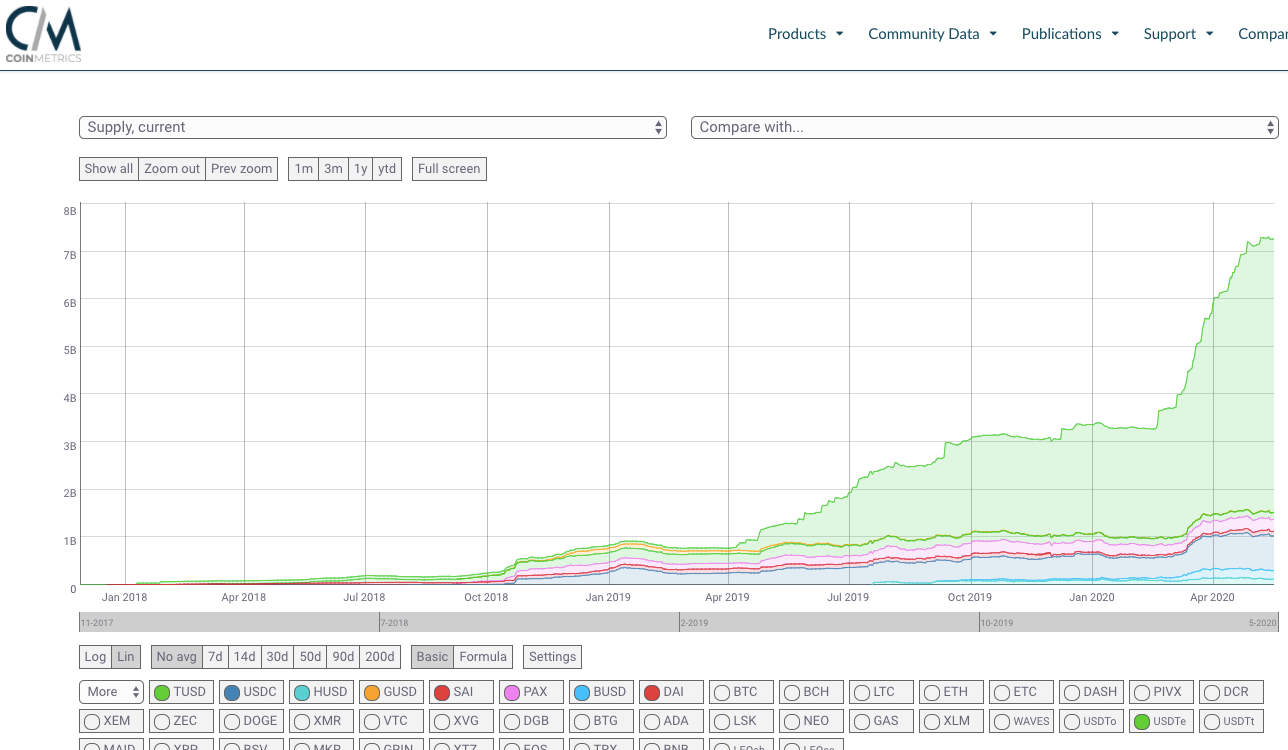

But the market isn’t waiting around for the central banks. In a critical but an early sign of product-market fit for DeFi, USD-denominated stablecoin issuance on Ethereum is up over 100% since the Covid market correction in March, a crisis largely attributed to a lack of liquidity.

What many confuse about DeFi is that they think DeFi adoption means the adoption of a cryptocurrency or other new types of currency as a medium of exchange (MoE), when in fact it means the use of *any* currency as a MoE. It just so happens that the most popular MoE currency in the DeFi economy today is USD, mirroring the dominance of the USD globally.

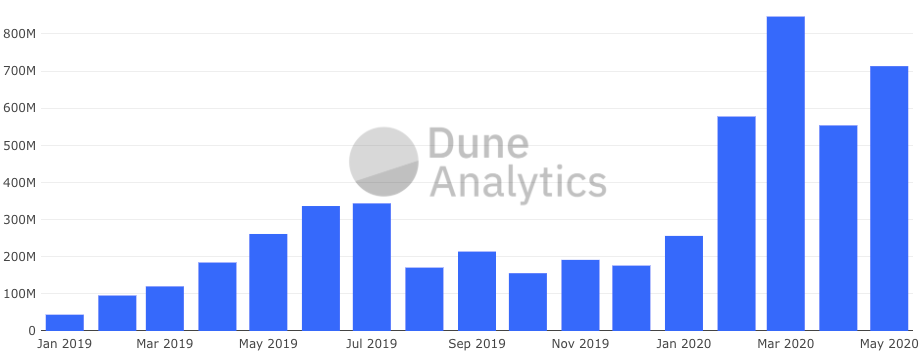

Decentralized trading infrastructure (DEX) is showing a similar growth pattern.

Stablecoin issuance and adoption of DEX infrastructure are important precursors to the adoption of the user-facing products being built by DeFi startups today. The liquidity in USD-denominated assets combined with the programmable and composable aspects of DeFi protocols ensures that all of the other programmable financial services that are being built on top will have access to liquidity, the key enabler for mainstream adoption of DeFi.

With infrastructure adoption beginning now but direct user adoption not yet here, it’s clear that the DeFi platform is still in its gestation phase on the Perez Curve. And you don’t need to be on the Midas List to figure out what comes next.

The Maturation of DeFi and Funding Cycles

So when will the institutional capital show up in DeFi?

To add the context of another macrocycle view, the current low tide is expected in what A16Z calls crypto’s “price innovation cycles”. Could it be as simple as institutional capital returns to the industry when the retail price of ETH rises again?

Many crypto VCs think so.

In an era where the market for negative yields is in the trillions and the stock market is drunk enough that *bankrupt* companies are this week’s hottest sector, anything is certainly possible.

While the above points to the numerous parallels between the post-dot com crash and the post-ICO crash, it’s worth noting here that some of the best vintages in venture capital history came out of that post-dot com crash when most institutional capital had left the space in a similar fashion.

What has to happen in legacy fintech for VCs to recognize the value of programmable finance?

Regardless, DeFi adoption is coming. But by that point, many of the fund-making return opportunities may be gone, by way of the value accrual models in DeFi. VCs will have to learn to get comfortable again with the risk associated with true early-stage investing to realize these rare returns that they spend their careers in search of.

There’s no small degree of irony that the same VCs who were snickering at all the unwashed masses underestimating the difficulty in early-stage investing during the ICO bubble are also the ones missing the emerging platform opportunity that came out of it.

Action steps

- Consider where DeFi is in the technology adoption cycle

- How you can capitalize on DeFi opportunities before the VCs figure this out?

(I like the crypto money portfolio composed of three types of bets)

Author Bio

Jonathan Joseph (JJ) is the founder of Smart Money, a DeFi studio. Previously JJ was the founder of FantasyIQ, an API for fantasy sports startup, and a venture capital investor at In-Q-Tel.

Subscribe to Bankless. $12 per mo. Includes archive access, Inner Circle & Deal Sheet.

🙏Thanks to our sponsor

Aave

Aave is an open source and non-custodial protocol for money market creation. Originally launched with the  Aave Market, it now supports

Aave Market, it now supports ![]() Uniswap and TokenSet markets and enables users and developers to earn interest and leverage their assets. Aave also pioneered Flash Loans, an innovative DeFi building block for developers to build self-liquidations, collateral swaps, and more. Check it out here.

Uniswap and TokenSet markets and enables users and developers to earn interest and leverage their assets. Aave also pioneered Flash Loans, an innovative DeFi building block for developers to build self-liquidations, collateral swaps, and more. Check it out here.

Not financial or tax advice. This newsletter is strictly educational and is not investment advice or a solicitation to buy or sell any assets or to make any financial decisions. This newsletter is not tax advice. Talk to your accountant. Do your own research.

Disclosure. From time-to-time I may add links in this newsletter to products I use. I may receive commission if you make a purchase through one of these links. I’ll always disclose when this is the case.