| 24h Majors & Movers | ||||||

|

BTC $59.5k | ↘ 5% |

|

HYPE $59 | ↘ 4% | |

|

ETH $1.5k | ↘ 6% |

|

CELO $0.06 | ↗ 4% | |

|

SOL $65 | ↘ 5% |

|

AAVE $73 | ↗ 2% | |

Enjoying this article?

Subscribe to Bankless or sign in

- 🎈 Kraken's Ink L2 is moving its production infrastructure to Optimism's OP Enterprise Fully Managed stack under a multi-year agreement, meaning

Optimism will now operate Ink's chain on Kraken's behalf.

Optimism will now operate Ink's chain on Kraken's behalf. - 🔮 Kalshi has sued Illinois over a new state law that would require the platform to obtain an Illinois license and pay a 0.2% privilege tax on digital asset transactions, arguing that federally regulated event contracts are outside the state's jurisdiction.

- 🏦 Maryland Democrat Adrian Boafo won Tuesday's Democratic primary for retiring Rep. Steny Hoyer's open House seat, powered in large part by $5.5M in backing from Fairshake, the crypto industry's top PAC.

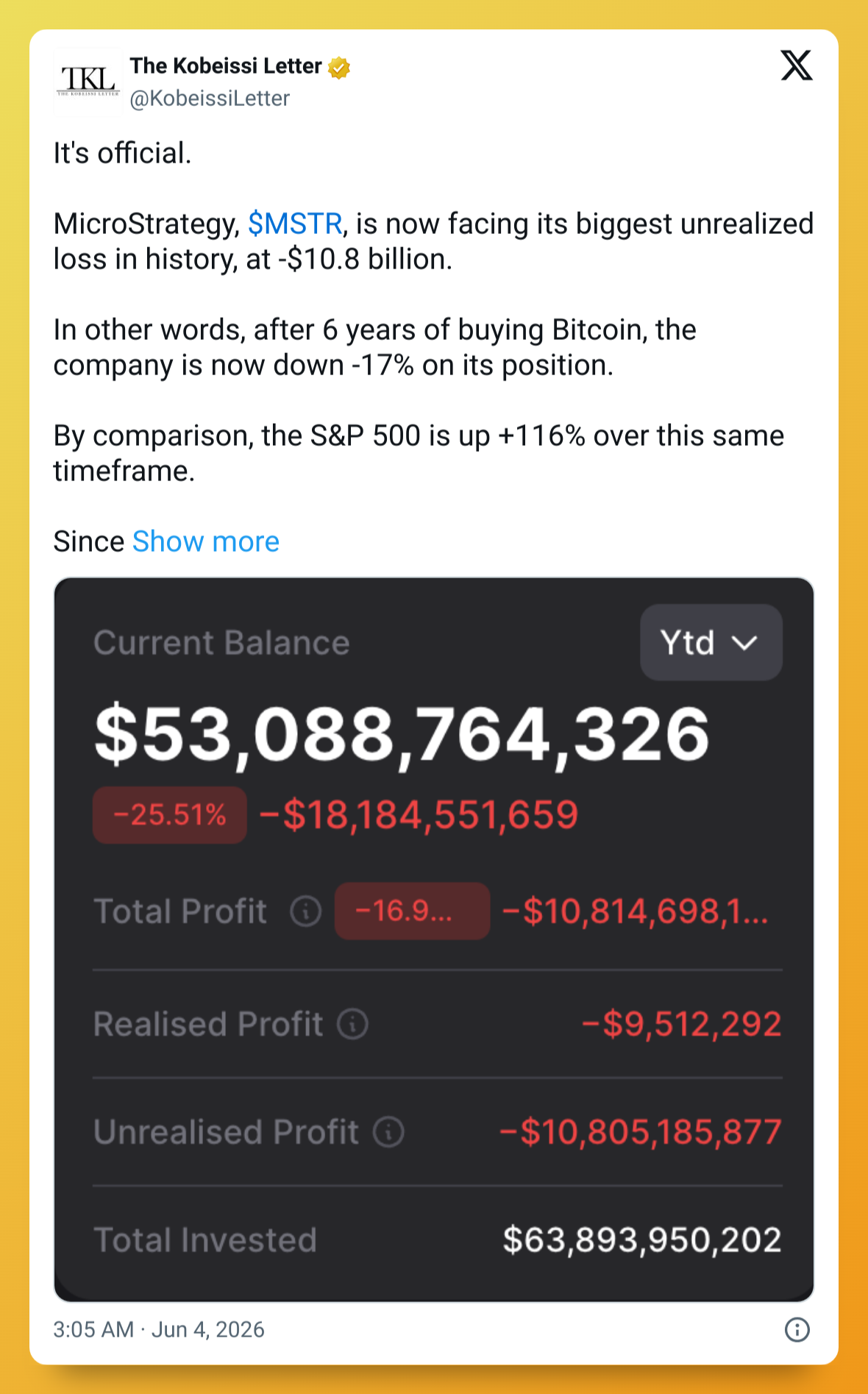

Today, the brightest red streak runs through Michael Saylor's Strategy, where its STRC preferred has fallen to around $80, a record discount to its $100 par. MSTR is breaking lower, below $100 for the first time since March 2024, and Bitcoin has slipped under $60,000.

This has been building since late May, when Strategy repurchased debt, sold a token amount of Bitcoin to cover preferred distributions, then kept buying more even as confidence in STRC cracked.

Today is just where the warnings converged.

Three Parts of the Machine

Strategy's structure runs on three pieces that lean on each other: Bitcoin, MSTR common stock, and the STRC preferred.

- Bitcoin is the reserve asset, the third largest on earth, and the pitch is that it only grows. Yet, it produces nothing, no dividend, no interest, no income. Strategy can hold it forever, but the preferred dividends are paid in cash so something needs to bridge that gap. That's the mismatch now being tested.

- MSTR is the engine. When the stock trades above the value of the Bitcoin behind it, Strategy sells shares to buy more, and the premium makes the buying accretive. When MSTR falls, the engine gets expensive. Raising $500 million at $500 a share takes 1 million shares. At $50, it takes 10 million. Same cash, ten times the dilution, eroding the reason to hold MSTR at all.

- STRC is the credit leg, a preferred stock with a $100 stated value paying an 11.5% cash dividend. Strategy can lift the rate to draw buyers when it slips. That works only while investors trust the dividend will keep coming, and that runway is shrinking. A price near $80 says the market wants far more yield before treating STRC like par.

Each piece holds up the others, so when all three weaken at once, the question shifts from how much Bitcoin Strategy owns to whether it has the dollars to keep its word.

The Current Conundrum

Strategy is losing trust and liquidity at once, and the two feed each other.

As Bitcoin falls, MSTR falls harder, because the market treats it as leveraged Bitcoin. As MSTR falls, selling stock to raise cash gets uglier, throwing the weight onto the reserve.

The STRC dividend bill has reportedly climbed from about $300 million a year in January to roughly $1.2 billion now, while cash dropped on debt buybacks and BTC purchases. Runway for those payments has fallen from more than seven years to about 14 months.

That's the trap and, while exits exist, each has its toll.

- Buying more Bitcoin undermines cash reserves, eroding trust in STRC.

- Issuing MSTR means heavier dilution, which means less reason for people to hold MSTR.

- More preferred adds more dividend obligations, and raising the STRC rate deepens the cash drain.

Payments can't be stopped because that would break the trust and the whole system. The whole structure runs on it, so effectively we’re left with selling Bitcoin.

Why Selling Bitcoin Cuts Both Ways

Selling would refill the reserve fast. Strategy could fund dividends, even buy back STRC below par, retiring a $100 claim for around $82. On a spreadsheet, it's rational. Analytics firm CryptoQuant puts the need at about $2.8 billion to restore 24 months of coverage, roughly $1.4 billion above the current reserve.

That’s a lot of Bitcoin to sell.

And Strategy has already tested this door. On June 1st, it announced it had sold just 32 BTC for about $2.5 million, a rounding error against more than 840,000 BTC. Since then, MSTR is down ~38%.

The reason to own MSTR is that it almost never sells, a leveraged Bitcoin bet whose stack is supposed to be permanent. The moment Strategy sold coins to pay its own preferred, the treasury stopped being untouchable and became a funding source for the structure on top of it. That reframes every future shortfall: if a $2.5 million sale was acceptable, a larger one is no longer unthinkable.

Selling now also turns paper losses into real ones. CryptoQuant estimates Strategy is underwater by about $10.6 billion on coins bought across 2024 to 2026. Hold, and the losses stay theoretical. Sell near these levels, and they lock in. Yet, the cleanest fix is the one that confirms the fear.

To be clear, this isn't Saylor emptying his clip tomorrow.

Strategy still has cash, can still issue stock and raise STRC's dividend, and Bitcoin can still rebound. The machine doesn't break today.

But the trajectory has darkened. The sequence since late May, debt buyback, a symbolic sale, more issuance, more BTC, and STRC still slipping, seems like a structure running out of easy answers.

The bull case is that Bitcoin rebounds, MSTR recovers, STRC's yield draws buyers, and the flywheel restarts. But a structure investors trust only because it can still dilute, pay more, or sell Bitcoin has already lost its fire.

The bear case is harder to shake. Strategy has bought time with issuance and more Bitcoin while the dividend bill compounds, and the obvious remedy, stop buying and rebuild cash, throttles the only engine the story runs on.

That's Saylor's bind. Sell Bitcoin, and he undermines the permanent-accumulation thesis that made MSTR what it is today. Refuse, and the strain lands on dilution, payouts, and the reserve instead. Neither path is clean, and both could pressure confidence in Strategy and in the wave of treasury companies built on the same idea.

Yet, sometimes the most painful path forward is the one that must be taken. Here’s to hoping better scenarios will prevail.

Bitget’s Stocks 2.0 brings 500 major equities and ETFs (like Tesla and NVIDIA) directly to your portfolio. Enjoy 1:1 mapping, deep liquidity, and USDT dividend payouts with ultra-low 0.04% fees.