Subscribe to Bankless or sign in

Level up your open finance game three times a week. I’m releasing this Free for Everyone until November 1. Get the Bankless program by subscribing below.

Dear Crypto Natives,

It’s Tactics Tuesday! Really excited about this two part tactic.

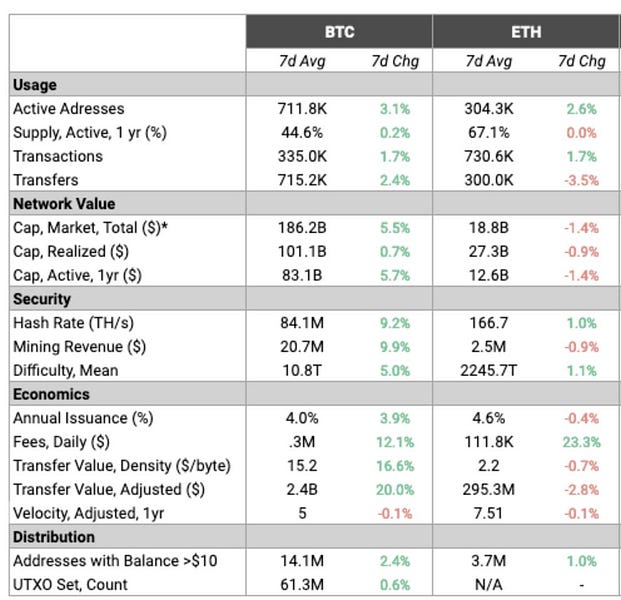

The public data produced by crypto money ledgers provides a lot of clues on the traction and growth of these systems. It’s there for everyone to see.

Subscribe for free to continue reading

- Support the Bankless Movement

- Access to thousands of articles

- Complete archive of Bankless episodes

- Embark on free quests in Airdrop Hunter

- Daily alpha in your inbox

Already subscribed? Sign in