Subscribe to Bankless or sign in

Dear Bankless Nation,

Last week, Jordi Alexander wrote a piece in the Bankless Newsletter titled Is the Merge Overhyped?

Ever since Jordi came on Bankless and helped us unpack the ticking time bomb that was Terra (about a month before it collapsed), I’ve enjoyed his rational and sober thoughts on the market. Reading his bear case for the Merge was a great exercise, one which I certainly have a hard time seeing on my own.

However…

I think there are some big things that Jordi either got wrong or overemphasized!

I’ve written some rebuttals to the parts of Jordi’s piece which I think needed them the most.

Tl;dr:

- Bearish because of low gas fees? Don’t be; it’s the issuance reduction that’s the big deal.

- Bearish because of the locked ETH overhang? Maybe… but I think this is overstated.

- Bearish because yields are going to be low? Don’t be; that’s actually the bull case that we’re looking for.

Let’s dive in.

Is the Merge Overhyped?

Argument 1: It’s just a narrative play

Jordi’s first argument is that ‘this is yet another narrative trade opportunity, in an endlessly long line of crypto narrative trading opportunities’. Baked into this argument is the idea of “it doesn’t matter how fundamentally strong the catalyst is, the market can always front-run the opportunity faster than the catalyst is strong.”

I think this is a cop-out argument. This is just saying that any and every event will be forgotten by time, and we’ll be on to the next narrative once it’s over.

This leaves no possible room for anything about the Merge to be fundamentally bullish. It’s shutting the door before we’re even discussing the merits.

“Lalala, doesn’t matter, sell the news”.

IMO, the counter-argument to this is easy.

The  Ethereum merge is one of the most significant events in crypto’s history since the genesis of Ethereum itself. Not only that, but it’s also one that’s fundamentally about price and value.

Ethereum merge is one of the most significant events in crypto’s history since the genesis of Ethereum itself. Not only that, but it’s also one that’s fundamentally about price and value.

If there’s ever going to be something significant enough to break through the ‘traders gonna trade’ mimetic, it’s the Ethereum merge.

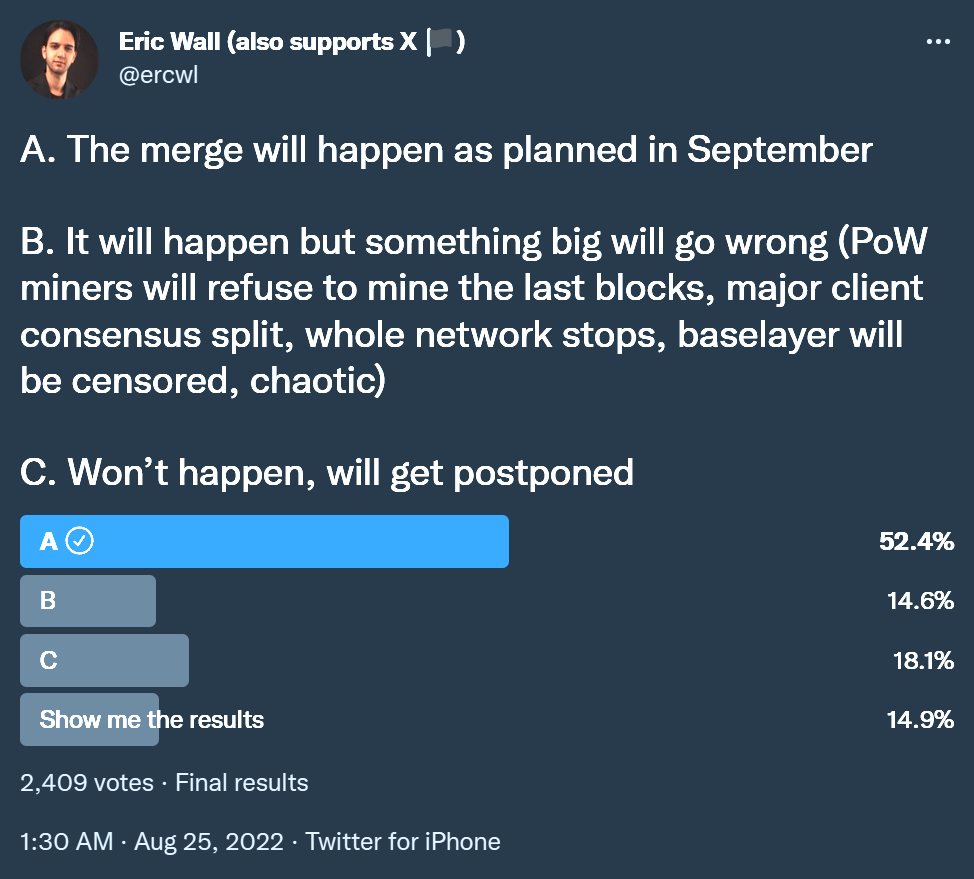

If you don’t believe this sentiment, check out this Twitter poll from Eric Wall:

Just over half say the Ethereum Merge will happen as advertised. Another 32.7% say either something will go wrong, or it won’t happen.

That’s 62% saying the Merge is going to happen, and 38% saying it won’t or something will go wrong.

Now, if you’re like Me, Ryan, Anthony Sassano, or any of the Ethereum client teams and core devs, you think there’s a >95% chance of the Merge happening on September 15th, and it being a complete success.

If the market is pricing in less than 95% success, then I claim that the Merge isn’t priced in.

Place your bets I guess, but it’s worth noting that the people who are experts on the details of the Merge are more bullish on its success than the people responding in this poll.

Eric Wall’s Twitter following is also a wide variety of many different communities, so while Twitter polls aren’t great data tools, I think this is an anomaly that accurately reflects a wide distribution of communities

Argument 2: Gas fees are down bad

Jordi’s next argument is that gas fees are down bad.

He’s right, they are.

“During the last 30 days in the month of August, during which ETH price has been up over +50%, the gas burn has been a mere ~1,300 ETH per day.”

Through this, the burn rate from EIP 1559 becomes negligible, creating a headwind on the narrative that ETH becomes ultra sound money. 🦇🔊

He also argues that gas fees will never return to DeFi Summer or NFT Mania levels. Both smart contract and NFT sale mechanisms have become much more efficient and gas optimized, and also the L2 ecosystem is far more developed and ready to soak up a lot of L1 blockspace demand.

He’s right!

I can totally get behind Jordi’s argument that the days of 200+ gwei gas prices are over.

But I also think that the current paradigm of 8-12 gwei average gas prices is also low. We’re in a bear market. We’re hungover from 2021. There are not many new things happening.

Gas prices will once again return as soon as any semblance of price action also returns to crypto. There’s always a new thing to do. There’s always another bull market on the horizon.

Jordi’s argument that 200+ gas fees are an anomaly; my argument is that 8-12 gwei gas prices are also an anomaly.

Enjoying this article?

Subscribe to Bankless or sign in

And we only need 15 gwei to be net negative on ETH issuance.

BUT MUCH MORE IMPORTANTLY, THIS WHOLE THING IS OVERSTATED.

The Merge is about the issuance reduction in block rewards! It’s not about the burn!

10 Gwei gas prices burns ~1,000 ETH a day.

Proof of Stake removes about ~13.5k ETH issuance per day.

Who gives an F about the low gas prices; the issuance reduction has always been the faster horse. The burn is just the cherry on top. This effect is why some ETH bulls are expecting to see the Merge’s impact on ETH price relatively quickly; months not years.

When ETH’s issuance reduction goes down to 0.43%, are we really going to say it’s not bullish when the rest of the L1s look like this?

Argument 3: Locked Staked ETH will Dump

Jordi’s next argument is that the supply of staked ETH and its rewards will hang over the market. In turn, the possibility of significant sell pressure once the unlock happens is scaring investors.

Maybe the narrative of this is true, but the actual facts behind this narrative don’t appear very bearish to me.

First and foremost, PoS is a system that inherently rewards those who are most bullish on the asset.

Some people began staking their ETH on the beacon chain early in the 2021 bull market; while ETH was just $400-$700 or so.

Question for you; are these people:

- Itching to lock in their profits?

- Perma-bulls who were willing to take the unknown lockup period by staking ETH early and are likely never-sellers?

If you staked your ETH while ETH was still below $1,000, you did it in the first ~6 weeks that the beacon chain went live. You willingly took on an unknown amount of lockup time, for ~6-7% yield on your ETH.

Psychologically speaking, I don’t see this population of people being eager ETH sellers.

If you are a low-conviction ETH staker, who wanted a liquidity exit door, they would have staked with Lido, which launched the same month as the beacon chain, and therefore you’ve been able to sell your stETH at any time.

And even at current prices, ETH has gone up 2-4x for the earliest stakers. It’s not the 10-100x gains of private token markets that actually do move token prices downwards.

Finally, the opening of a sell gate can also be mitigated by the equal-and-opposite ETH buying pressure from those who are waiting for the merge to de-risk Ethereum and buy ETH once the merge is in the rearview mirror.

Argument 4: Yield will go down

Jordi argues that ETH staking yields are coming down bigly.

In a year when those risks are behind, ETH staking Mall Cops will be lucky to be earning 1–2% APY after token inflation, even lower than US treasury bonds.

In 2023, we will see somewhere between 30 and 60M ETH staked

Wait, is this bearish?

Because this is actually the same thing as my bull case.

If the ETH yield has gone down so low, it’s because a significant amount of ETH has begun staking, and the issuance is spread out among a wide set of participants. This is what an ETH bull would want to see.

Low ETH yield means that there’s a ton of locked up ETH. There’s a lower and lower float as more and more ETH gets staked.

It also means that ETH yield in DeFi is also strong, meaning that DeFi has also sucked up a lot of ETH from the secondary market too.

I find it hard to see 30m to 60m of ETH staked, and it also being bearish. A high supply of staked ETH has always been one of the core pillars of ETH value accrual, no matter what the associated yield on the ETH.

If people are willing to accept lower and lower yields on their ETH, to the point that yields drop down below 3%, it’s because the asset is extremely desirable, and owners are willing to be paid less to own it.

Also, if we’re worried about a supply overhang from the Merge, why are we also seeing the supply of staked ETH grow from 14m where it is today, to 30 to 60m ETH in 2023?

Doesn’t seem very bearish to me.

But what do I know, I’m just an ETH permabull. ¯\_(ツ)_/¯

Happy Monday.

- David

P.S. Is Ethereum about to get censored?!? We dropped a new episode with  Justin Drake talking about the biggest threat to Ethereum. Must listen.

Justin Drake talking about the biggest threat to Ethereum. Must listen.

Action Steps

- 🤑 Execute any good market opportunities that you saw

- 🎙 Listen to Ethereum Uncensored with Justin Drake