Dear Bankless Nation,

With crypto markets surging over the past couple days, it might be easy to forget just how uncertain everything felt a good 48 hours ago.

Today, we dig into USDC's chaotic depeg over the weekend, and how the overall stablecoin and DeFi markets reacted to it.

- Bankless team

A Look At The March 2023 Stablecoin Panic

Bankless Writer: Ben Giove

The collapse of Silicon Valley Bank on March 10 sent shockwaves through the crypto ecosystem, when Circle, the issuer of USDC, announced that they had $3.3B in deposits (roughly 8% of their backing at the time) at the bank.

This announcement caused a panic among holders of USDC, which de-pegged significantly as backers feared that there would be a run on the stablecoin if ![]() Circle was unable to be made whole on its SVB deposits.

Circle was unable to be made whole on its SVB deposits.

Jack gave an excellent breakdown of the crisis and its resolution yesterday, so I won’t give you another play by play. Instead, we’ll take a look at how the markets and DeFi reacted to the crisis. In particular, we’ll try to answer some questions such as:

- Which other stables depegged (to either the upside or downside)?

- How did this crisis affect DeFi?

- Did anything break?

Let’s dig in so we can answer these questions.

What De-Pegged, What Traded at a Premium?

We all know that USDC de-pegged, having traded as low as $0.80 on some venues, but it was not the only stablecoin to experience instability over the weekend.

Just about every other stablecoin endured well above average volatility between March 10-11, whether it be to the upside or the downside. I never thought I’d say this - but let’s touch on some of the noteworthy stablecoin price action below.

DAI

DAI, crypto’s fourth largest stablecoin is 43% collateralized by USDC via the peg-stability module (PSM) and G-UNI LP positions. The stablecoin traded as low as $0.886 during the panic, with the market fearing that it could be at risk of becoming undercollateralized should USDC continue to fall in value or experience a run.

The price of MKR, the protocol's governance token, also plummeted on the back of these fears, falling 26.1% as traders were likely anticipating a potential need for the token to be minted in order to serve as a backstop to satisfy redemptions.

FRAX

FRAX, the sixth largest stablecoin, is also collateralized in part by USDC through its liquidity and lending AMOs (algorithmic operations).As a result, FRAX experienced its largest ever de-peg, trading as low as $0.877 on some venues as the market feared it would be caught up in USDC-related contagion.

Like Maker, the protocol's governance and seigniorage token FXS, also fell significantly, dropping 20.4% from March 9-11. This decline is likely due to trader concern that a USDC implosion would result in FRAX redemptions, which in turn would lead to the minting, and subsequent sale onto the market, of FXS.

USDT

The largest stablecoin by market cap, ![]() Tether has come under heavy criticism for its opacity relative to its competitors. However, perhaps due to its perceived limited exposure to the US banking system, USDT acted as a safe haven during the crisis. The stablecoin largely traded near, and at times even above, peg.

Tether has come under heavy criticism for its opacity relative to its competitors. However, perhaps due to its perceived limited exposure to the US banking system, USDT acted as a safe haven during the crisis. The stablecoin largely traded near, and at times even above, peg.

DeFi users even “fled to USDT” pulling it from liquidity pools and lending rather than risk exposure to USDC or USDC-exposed assets such as DAI and FRAX (more on this later).

LUSD and sUSD

Liquity’s LUSD and Synthetix’s sUSD both traded at premiums throughout the crisis, with both trading as high as $1.08 on some DEXs during the height of the panic. Like USDT, these assets were utilized as safe havens during the crisis. However, rather than value its lack of ties to the United States, the market placed a premium on each stablecoin's exclusive use of crypto collateral.

Enjoying this article?

Subscribe to Bankless or sign in

In the case of Liquity, this would be ETH, as LUSD can only be minted from this trustless bearer asset. Despite sUSD utilizing SNX, and not ETH, as collateral, traders still greatly valued its decentralization properties during the crisis.

![]() Across is the bridge you deserve: fast speeds, low fees, great support, no hacks, and we love our users. Try it once and you’ll understand why Across users love us back and have bridged $billions with it.

Yield farmers will also find attractive yields for providing bridge liquidity! 👀

Across is the bridge you deserve: fast speeds, low fees, great support, no hacks, and we love our users. Try it once and you’ll understand why Across users love us back and have bridged $billions with it.

Yield farmers will also find attractive yields for providing bridge liquidity! 👀

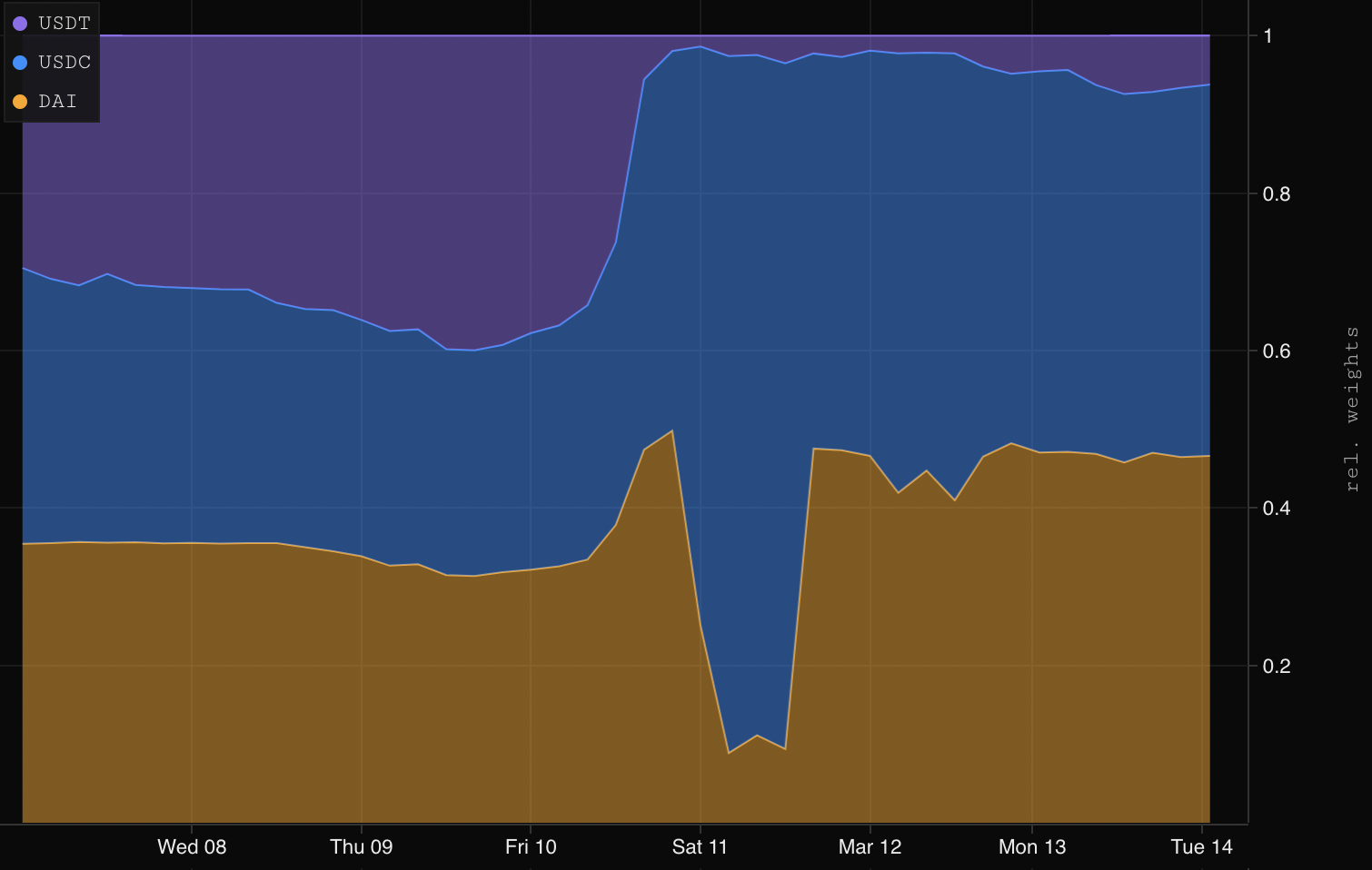

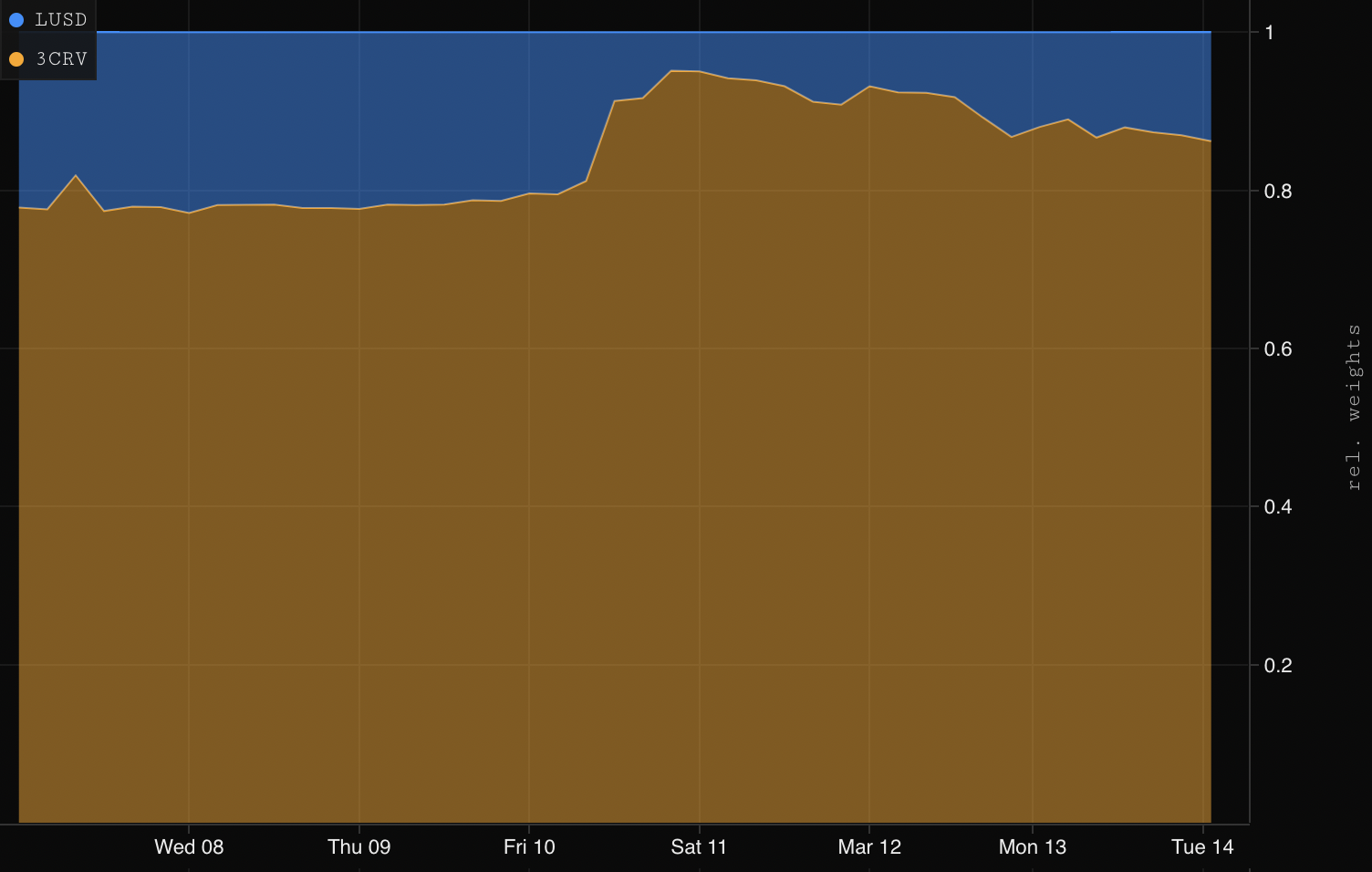

Curve Pools

Curve pools serve as sources of deep liquidity for stablecoins, as they have proven highly attractive to LPs due to the low risk of impairment loss in like-asset pools as well as the ability to earn CRV emissions. Curve pools also serve as a gauge (pun intended) on how the market views the risk of a given stablecoin. As pools becoming imbalanced (i.e., not having an equal ratio of each stable), it can indicate what assets LPs view as more or less risky.

With this in mind, let’s take a look at how the composition of Curve pools changed during the crisis starting with the 3Pool, the largest pool on Curve which consists of USDT, USDC, and DAI.

As we can see, LPs fled to USDT during the height of the panic, seeking to reduce their exposure to USDC and DAI. During the peak of the panic on the night of March 10, the 3Pool became heavily imbalanced, holding just 1.5% USDT. On March 11, liquidity providers sought to further decrease their exposure to USDC by draining the pool of DAI, which had as low as an 8.5% composition of the pool.

Considering that the 3Pool is in theory supposed to have ⅓ of each stable, this is a massive imbalance. Although it’s recovered somewhat, as of writing the pool continues to remain heavily imbalanced, with a composition of 47.1% USDC, 46.6% DAI, and 6.3% USDT.

Stablecoin holders in other pools sought to flee USDC as well. For instance, the LUSD pool had a high imbalance of 95.5% USDC compared to just 4.5% LUSD.

The through-line is clear - liquidity providers fled stablecoins that were exposed to USDC towards ones that were not. Although they have become more so, the pools remain heavily imbalanced against USDC, suggesting that some fear remains in the market.

Lending Markets

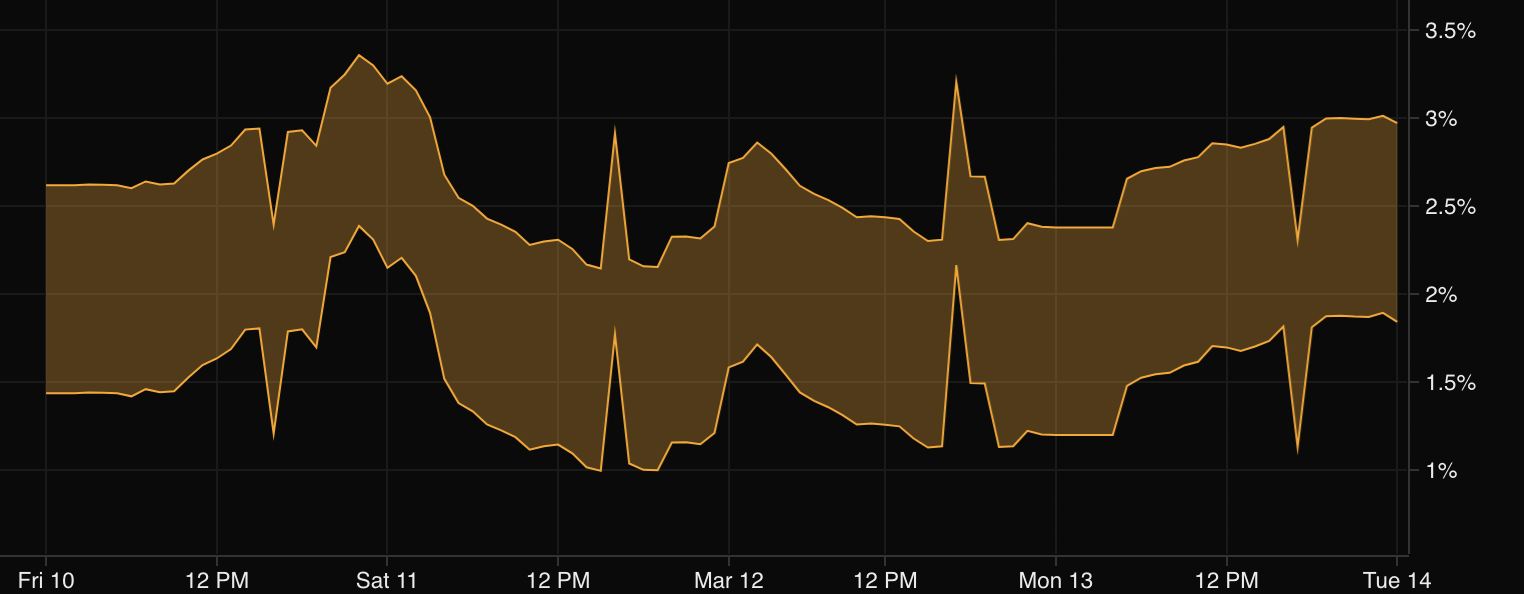

Now, let’s see how lending markets reacted to the crisis.

Aave V2 Rates 3/10-3/14 - Source: Parsec

Aave V2 Rates 3/10-3/14 - Source: ParsecThere was significant volatility in interest rates in both directions on these markets, with borrow rates for USDC plummeting from 3.4% to 2.1% on Aave V2 on Ethereum. Rates for DAI followed a similar trajectory, falling from 2.9% to 0.9%.

Notably, interest rates for stablecoins that traded near peg or at premium like USDT, LUSD, and sUSD soared during this period. For instance, borrow rates for LUSD rose as high as 75% on March 11, with utilization for the asset soaring during this time.

While at first glance it may appear as though borrowers were shorting these latter stablecoins, in reality the high rates are likely due to users pulling these assets in order to get out of Aave, which had heavy exposure to USDC and DAI. This means that during the crisis Aave experienced a mini-run of its own, but unlike meatspace banks such as SVB, the protocol continued to operate without issue.

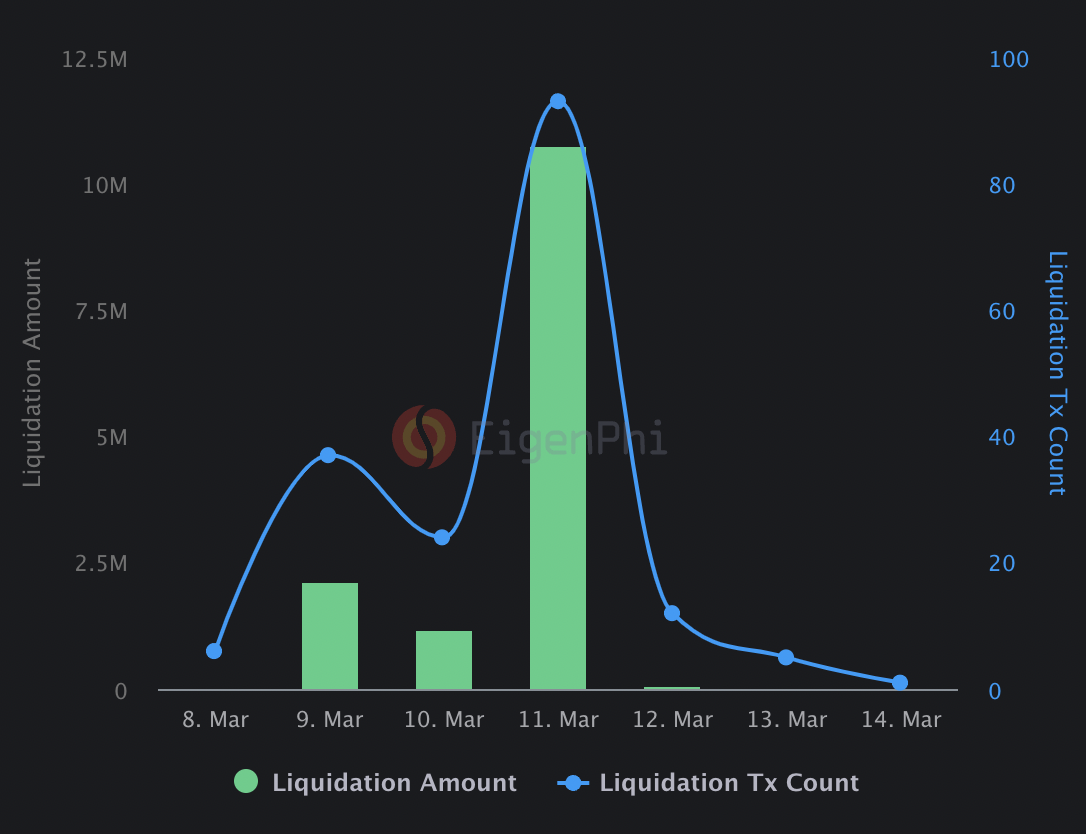

Ethereum Liquidations - Source: EigenPhi

Ethereum Liquidations - Source: EigenPhiAlong with withstanding a “mini-run”, lending protocols like Aave were able to facilitate liquidations without a hitch amidst the volatility. Per MEV analytics site EigenPhi, there were more than $11.9M in liquidations between March 10-11, with major lenders like Aave (both V2 and V3) and Compound sitting on just ~$800K of bad debt. This accounts for just 0.014% of the combined TVL across these protocols.

Did Anything Break?

So, with all of this instability in stablecoins… did anything break?

The answer is, not really. Although liquidity providers fled to non-USDC stablecoins, no protocols “broke” as a result of the de-peg. As it’s been throughout the bear market, DeFi was resilient, facilitating liquidations that resulted from the volatility -- lending protocols accrued little bad debt as a result of the crisis.

Despite this, there are lessons to be learned from the crisis. First and foremost, it’s become clear that DeFi must reduce its dependence on fiat-backed stablecoins that are beholden to the fragility of TradFi. It also revealed potential vulnerabilities.

In addition, the panic demonstrated that decentralized assets command premiums during times of crisis. While we saw a “flight to safety” with the price of BTC and ETH actually increasing from March 10-11, and stablecoins like LUSD and sUSD, which are both backed solely by crypto collateral, traded at premiums over the weekend.

Action Steps

- 📖 Read yesterday's article How a Few Banks Lost Everything All at Once